We wish to advise that the C65 and C66 tables have now been discontinued. The final publication is today, the 13th April 2021. An additional Stats Insight .pdf file has been included as part of this final release.

Bank customer lending flows capture new credit events during the course of a week. The data files attached include weekly metrics for housing (loans fully secured by residential mortgage), business, and consumer finance lending.

C65 and C66 discontinued

7 April 2021

The bank customer lending collection was introduced as a temporary data collection in late March 2020. Its purpose was to monitor the impact of COVID-19 on the banking sector.

We wish to advise that the weekly survey which collects data for the C65 and C66 tables is now being discontinued.

The final publication of the C65 and C66 tables will be on 13 April 2021. This publication will include data for the week ended 2 April 2021.

The data: coverage, periodicity and timeliness

Coverage characteristics

The table shows aggregated data from the weekly Bank Customer Lending survey that is completed by 13 registered banks in New Zealand.

The Bank Customer Lending survey introduced in late March collects financial information on bank customers to better understand the impact of COVID-19 and associated policy initiatives on households, businesses and the banking sector.

Periodicity

Weekly.

Timeliness

Weekly data is published on the sixth working day after the end of the preceding week.

Access by the public

Statistics release calendar

The statistics release calendar provides a plan of scheduled releases. We update and release it on the first working day of the month.

View the statistics release calendar

Integrity

Dissemination of terms and conditions under which official statistics are produced, including confidentiality of individual responses

We collect data under Section 93 of the Reserve Bank of New Zealand Act 1989 (the Act).

Read the Reserve Bank of New Zealand Act 1989

We only publish aggregated data. Individual institutional data is confidential.

Provision of information about revisions and advance notice of major changes in methodology

New data, or revised data, are in bold font. This applies to the summary table only and not Excel files. We generally publish revisions when the table is next due to be updated and released. Should we need to make revisions more promptly, we post a special note on the website. We post any major changes in methodology in a special note.

Bank Customer Lending metrics – Series description

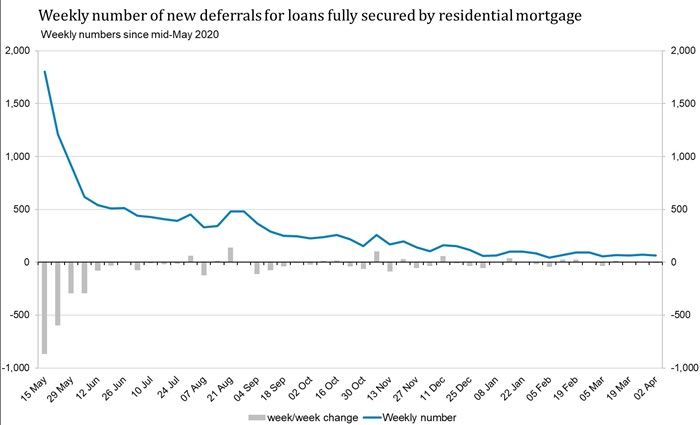

Loans fully secured by residential mortgage

Loans fully secured by residential mortgage includes loans secured by a mortgage over a residential property. This excludes loans cross collateralised between residential property and other assets where the share attributable to the residential property cannot be identified.

Restructured facilities to interest-only

Interest-only loans have no initial scheduled principal repayment, but may at a later date change to principal and interest. This does not include revolving credit loans that have a fixed limit or revolving credit loans that have a scheduled reducing limit. We collect the (confirmed) total number and total customer exposure of residential mortgage loans that are restructured to interest-only in the reference period.

Requests for mortgage deferral

This captures requests for principal and interest payment deferrals for up to six months on residential mortgage loans under the government package, announced Tuesday 24 March 2020, for customers whose incomes have been affected by the economic disruption from COVID-19. Each bank is likely to have its own eligibility requirements. A mortgage payment deferral is an agreement by the lender to allow the borrower to temporarily stop or reduce mortgage repayments. We collect the total number and the total customer exposure of residential mortgage loans where a repayment deferral request has been received.

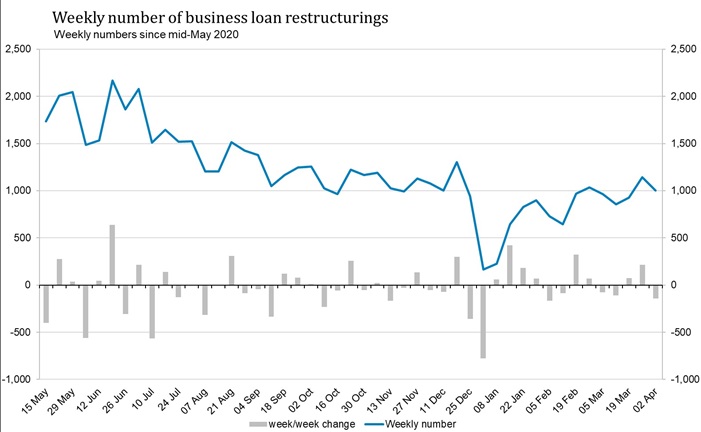

Business loan metrics

Business loans include loans to financial institutions and non-financial business (agriculture, commercial property and other businesses).

Restructured loan facilities (includes top-ups, extensions, interest-only, payment deferral)

Each bank is likely to have its own eligibility requirements. We collect the total number and the total customer exposure of business loan top-ups, extensions to term, interest-only and other payment deferrals.

Top-ups are increases in lending (regardless of purpose) to an existing loan where the underlying security has not changed but may be revalued and/or additional security may be provided. It is not an undrawn commitment.

Extensions to term includes a request to extend the term of a loan.

Interest-only is where the customer seeks relief by moving from principal and interest payments to interest-only payments.

Payment deferral is where the customer seeks a break from repayments for a specified period.

Business Finance Guarantee Scheme

On 24 March, the government announced a $6.25 billion Business Finance Guarantee Scheme. The government and banks implemented the scheme for small and medium-sized businesses, to protect jobs and support the economy in relation to the economic effects of COVID-19.

The Reserve Bank (RBNZ) has released new Bank Customer Lending metrics which provide more timely and detailed measures of the changes in lending to bank customers since the onset of COVID-19 in New Zealand.

The data has been collected weekly since late March 2020 from registered banks in New Zealand. Lending through other financial service providers, such as credit unions, is not included.

Why is the data collected?

The data is collected to obtain bank customer lending metrics on a timely basis in relation to the COVID-19 impact on the banking sector. The collection was set up to support prudential monitoring of the banking sector.

What is the data quality of the series being published?

We have assessed the quality of bank customer lending metrics data and concluded that the series we have chosen to publish are of sufficient quality for publication.

Data is provided to the RBNZ on a ‘best endeavours’ basis with improvements being made over time as coverage and definitions were refined in consultation with banks. This means that while we consider the data valuable for monitoring purposes, it is not fully aligned with the high rigour of statistical frameworks we usually apply to our official statistics. It will be subject to revision as required.

The series we have chosen to publish will still have some areas where improvements were seen over time. For example; “Missed payments” was initially defined as 1-29 days but changed to 7+ days from 17th April 2020.

What is the main use of the data?

The data will be of most value in assessing trends over time across the range of metrics.

What is the difference between flow data and stock data?

Flow data means new credit events, e.g. bank customers’ requests for new loans or changes to their existing loans during the course of a week (the reference period).

Stock data or ‘as at’ position shows lending at each point in time.

Can you add cumulative flows to get a stock position?

No.

Cumulative flows will be higher than the ‘as at’ position in part because the flows are only increases in credit events and not any decreases as customers move off schemes. Over time some treatments may have been applied and then removed and/or facilities may be repaid.

Also over time a customer may have repeated counts as they flow into one treatment, then out and back in. For example; a customer may request a mortgage deferral, then revert back to principal and interest payment and then change to interest only.

Is there any double counting in the data?

Yes. There will be double counting in some metrics as customers move between support schemes.

For example, in the restructured business loans; a customer may one week request a temporary overdraft and put a principal and interest loan onto interest only. They may then come back the following week to request deferred payments. This scenario would count each of those as separate events in the weekly reports as they occurred.

How are missed payments defined?

A missed payment is defined as 7+ days after due date. In the week, we seek the total number and total value of loans that have missed payments. We seek the total exposure to the customer. This is not the sum of the value of missed payments during a week.

Is RBNZ publishing data that is already published by the New Zealand Bankers Association (NZBA)?

The NZBA is publishing Business Finance Guarantee Scheme (BFGS) loans showing the amounts for new lending representing limits of limit increases. RBNZ will data will show a further breakdown of this lending by categories such as drawn and undrawn lending.

Balances may differ slightly as reporting periods may differ by a few days.

Some other series may have a cross over with other data published by NZBA without a direct comparison.

How long will this data collection run for?

We set up a new weekly survey to collect this data, but we do not intend it to be a permanent addition to our suite of surveys. The frequency and content of this survey will be reviewed on an ongoing basis.

Why are you choosing to publish this data now?

This collection was initially set up for internal monitoring purposes, on a “best endeavours” reporting basis. The data has evolved and improved since the collection began. We have reviewed data quality and assessed selected series as being fit to publish.

Symbols and conventions for summary table

| Symbol or convention | Definition |

|---|---|

| 0 | Zero or value rounded to zero |

| - | Not applicable |

| .. | Not available |

| bold | Revised/new |

| italics | Provisional |

| Light grey background | Historical |

General notes

- Individual figures may not sum to the totals due to rounding

- Percentage changes are calculated on unrounded numbers

- You are free to copy, distribute and adapt these statistics subject to the conditions listed on our copyright page.