Panel remarks delivered to the Institute for Monetary and Economic Studies (Bank of Japan) in Tokyo

On 30 May 2019

By Christian Hawkesby, Assistant Governor and General Manager of Economics, Financial Markets, and Banking

Prepared with Cameron Haworth and Omar Aziz

Introduction

Tena koutou katoa

Thank you for the opportunity to talk about the Reserve Bank of New Zealand and the changes we are making to maintain our credibility in times of change.

I would like to focus on two building blocks of credibility:

- renewing a social licence to operate by aligning our objectives with the needs of the public; and

- achieving those objectives through good decision making enabled by a framework of good governance.

A common theme is the importance of transparency.

The imperative for change: Central banks in the 21st century

The first building block of credibility is the renewal of a social licence to operate—by this I mean the legitimacy an institution earns by serving the public interest. It is granted by the public when an institution is seen to fulfil its social obligations.1

New Zealand was the first country to officially adopt inflation targeting in 1989, with a number of central banks around the world following the example.2 Under a single-decision-maker model, we brought inflation down from around twenty percent to two percent in five years. In doing so, we helped build our credibility during the high-inflation environment of the times.3

Fast-forward to 2019, and monetary policy in New Zealand has undergone major change. Firstly, we have adopted a dual mandate, focused on achieving price stability and supporting maximum sustainable employment. Secondly, we have adopted a committee structure for decision making, and are delivering greater transparency in our decision making.

Why the change?

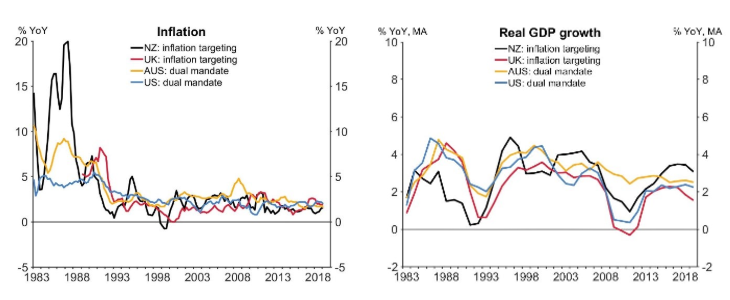

The reform of our framework was not merely a simple choice based on technical performance. As you can see in figure 1, when it comes to inflation and growth, over the past 30 years inflation-targeting central banks (e.g. New Zealand and the United Kingdom) have a pretty similar track record to central banks with a dual mandate (e.g. Australia and the United States). 4

The imperative for change comes from more than examining our history; it comes from our expectations of the future, and the present we find ourselves in. Our policy framework changed because times are changing. For the Reserve Bank to maintain its credibility and relevance, we must change too.

Figure 1: Inflation, and GDP growth across monetary policy frameworks5

Wellbeing of our people

Inflation has been low and stable in New Zealand for nearly 30 years.

There is a greater appreciation that low inflation is a means to an end, and not the end itself. In the fight to lower inflation that was perhaps easy to forget. The end goal is, of course, improving the wellbeing of our people.6

For many in the general public, employment is one tangible measure of wellbeing. Employment can provide an opportunity to earn your own wage, contribute to society, and live a fulfilling life.

It is in this light that the Reserve Bank Act (1989) has been amended to include a dual mandate with an employment objective alongside our price stability goal. Incorporating the objective of supporting maximum sustainable employment, and equally weighting it alongside inflation, emphasises our long-term goal of improving New Zealanders’ wellbeing. This aligns us with the needs of the public. And it helps us renew our social licence to operate - the first building block for maintaining our credibility.

But it is not enough for the public to believe in and understand our objectives. We must also prove to them that they can be achieved. This brings us to the second building block necessary for maintaining credibility: establishing modern governance principles for dealing with modern problems, and translating good governance into good decisions.

Good governance

In preparing for our dual mandate, and a formal Monetary Policy Committee (MPC), we have updated the principles and processes that form our governance framework for monetary policy.

In pursuit of greater transparency, we have also published these principles and processes in a comprehensive Monetary Policy Handbook (the Handbook). 7 This is an essential document, for everyone from school students to MPC members.

Importantly, it is also a living document that will evolve as our understanding evolves.

Principles

The first part of the Handbook I would like to cover is the section on MPC deliberation principles. 8

Figure 2: MPC deliberation principles

| Principle | Process Implications | |

| 1 | Clear objectives | Each meeting has a defined purpose and agenda. |

| 2 | Diversity | Inclusive of different intellectual and personal styles. |

|

3 |

Inclusion of information | Information and deliberation meetings expert-led (chaired by a senior expert with information presented by analysts). |

| Initial focus on understanding and discussing information; decision meetings clearly separated from information and deliberation meetings. | ||

| Inclusion of people | Decision meetings chaired by Governor. | |

| Deliberation meetings allocated enough time for discussion. | ||

| Clear avenues provided for expressing minority views. | ||

There are three principles which guide the deliberations within the MPC.

I’ve talked already about providing clarity around our objectives - the equal weighting of our employment and inflation goals. This is the first of our three principles.

The second, is diversity - diversity in the skills, experiences, thoughts, and personal characteristics of the MPC members.

The third, is inclusion - inclusion of information and people, ensuring decisions are made on the basis of all the available insights, and reflecting the views of all of the committee members.

Why are diversity and inclusion so important?

The governance literature shows that diversity and inclusion improves the pool of committee knowledge, insures against extreme views, and reduces groupthink.9 These principles drive the committee towards an unbiased policy decision - the best that is possible given existing information.

Think about this from a practical perspective. Modern monetary policy is confronted by diverse issues such as climate, technological, and other structural and social changes. A sole decision maker or uniform committee cannot possibly hope to possess the broad range of insights necessary to consider these issues.

A diverse committee operating in an inclusive environment can. It is these additional insights that improve collective understanding, and lead to better monetary policy decisions.

So you see these principles are not simply rhetorical devices. They are carefully chosen pillars to support our credibility though good decision making in achieving our dual mandate.

Good decision making

Processes

Our principles of good governance have directly influenced the policy-setting process of the MPC. 10 This is a process that has been designed with consensus-based decision making front and centre, consistent with the agreement with the Minister of Finance. 11

Figure 3: The structure of the forecast week for quarterly Monetary Policy Statements

| Monday | Tuesday | Wednesday | Thursday | Friday | Monday | Wednesday | |

| Staff present recent developments, issues, and risks. | Staff present outlook and strategy | MPC discuss risks and external messages | MPC discuss strategy and tactics | MPC decide on strategy and tactics | MPC finalise risks and external messages |

MPC decide level and direction of policy instrument MPS release |

|

|

Information - pooling |

MPC deliberations (Staff as advisers) |

MPC decisions (Staff not present) |

|||||

We begin with information pooling, which flows through to MPC deliberations, and culminates in the final decision making meeting.

As you can see, the policy-setting framework is highly collaborative and deliberate. Deliberate in the sense that the process inspires lively debate, giving MPC members every possible chance to challenge assumptions, critique policy judgements and assess a range of policy strategies to achieve our dual mandate objectives.

A crucial part of this is that the MPC members hold back their views on the decision until the final stages, rather than starting with them. This supports evidence-based decision making and guards against confirmation bias.

The process begins with open information pooling on recent developments and the outlook for the economy. Here, the MPC have the opportunity to investigate and challenge the assumptions made in the staff’s initial forecasts. This is where the MPC member’s judgement enters the picture, and where creative tensions improve collective understanding.

While the MPC members may enter the room with different insights and questions about the economy, at the end of the information pooling stage the committee shares a common reference point for the economic outlook.

There are numerous opportunities to discuss and reflect on key issues, judgements, risks, strategy, and communication throughout the week. There are also a number of anonymous internal surveys we perform to gauge collective opinion among staff and MPC members.12

By the end of the week-and-a-half, the final monetary policy decision reflects the greater momentum of the MPC’s discussion.

We publish the final Official Cash Rate (OCR) decision, a Monetary Policy Statement (MPS), and a Summary Record of Meeting at the same time.

The Summary Record of Meeting captures the key judgements and risks underpinning the central forecasts and decision, as well as indicating where members of the MPC had different views. We identify any differing views, and communicate where the most significant uncertainties lie in our baseline forecasts.13 If consensus cannot be reached, a vote by simple majority would be carried out, and the reasoning behind different stances disclosed in the Summary Record of Meeting.

Our desire is that the transparency provided in the Handbook can help the public understand how the Bank’s collective ‘mind’ works. If the public can see the analytical rigour in our decision making, they should have greater confidence in the MPC’s conclusions, and thus more faith in the Reserve Bank.

Our credibility will be supported in the long run if the decisions made by the MPC are unbiased and effective ones. Our results will speak louder than our words.

Monetary policy strategy and our May decision

So far I’ve talked about the principles and processes we follow in setting policy. Now I’m going to cover how we ‘walk the talk’ in formulating our monetary policy decisions.14

Sound and effective monetary policy strategy requires more than just deciding whether the OCR should go up or down on any given day; instead central banks need to be transparent about their views of the economy over the medium-term and how monetary policy might respond to a changing economic landscape.

In this regard, around twenty years ago, the Reserve Bank became a pioneer in another way. When publishing our interest rate decisions, we also began to publish a forward (and endogenous) projection of interest rates in the future. We use this to capture the overall stance of monetary policy.

This tool remains integral to how the MPC sets monetary policy and understands the potential trade-offs with a dual mandate.

The first monetary policy decision of the new MPC occurred last month, in May. Our starting point was a New Zealand economy where the labour market was operating near maximum sustainable employment, and annual core inflation pressures were within our 1 to 3 percent target range but below the 2 percent mid-point.

We discussed the slowdown in global growth, and how this might affect New Zealand. We also addressed the recent loss of domestic economy momentum since mid-2018, through both tempered household spending and restrained business investment.

In order to continue achieving our policy objectives, we agreed that additional monetary stimulus was needed to help bring inflation back to the 2 percent mid-point and support maximum sustainable employment. We then turned to the question of the magnitude of stimulus we wanted to adopt (the stance) and the timing and means by which we would try to deliver this (the tactics).

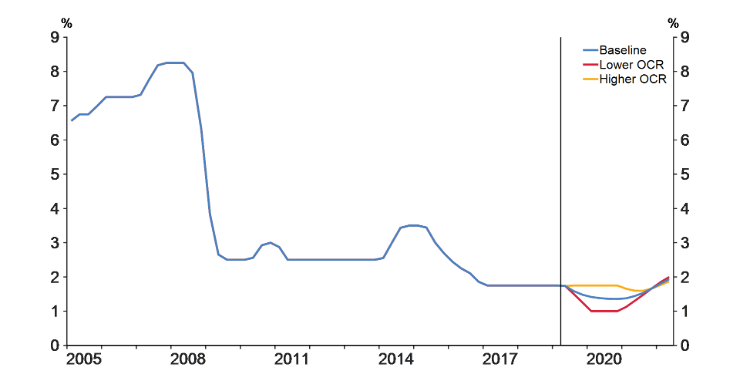

Figures 4–6 show how different OCR paths could have been used to achieve our objectives. While each path was consistent with meeting our objectives, they each offered different trade-offs.15

Figure 4: Official Cash Rate (OCR) paths to achieve alternative monetary policy stances

Figures 5-6: Inflation, and employment gap under alternative OCR paths

If we kept rates unchanged (the higher OCR path), our projections suggested that it would have taken a number of years for inflation to return to target, and employment would have fallen below the maximum sustainable level. If we lowered the OCR by around 75 basis points over the next 12 months (the lower OCR path), our projections suggested it would result is a situation where both inflation and employment would be overshooting their targets.

By contrast, the baseline (our final published projection), with the OCR around 40 basis points lower over the next 12 months, brought inflation back to target in a reasonable time period, with employment remaining near the maximum sustainable level. We decided this path captured our preferred strategy, and was robust to the key risks we had discussed.

After agreeing on the appropriate stance of monetary policy, MPC turned to the tactical decision of where to set the OCR at the May meeting, and decided to cut the OCR by 25 basis points to provide a more balanced outlook for interest rates.

This brings us to discuss the future.

Maintaining credibility in the future

Our central view is that New Zealand’s interest rates will remain broadly around current levels for the foreseeable future. However, we need to be ready to adapt to changing conditions, to meet our objectives even when confronted with unforeseen developments.

An issue that policymakers and academics are grappling with around the world is the role of both monetary and fiscal stimulus in a world of low interest rates.

There is emerging consensus that coordination is necessary for an optimal response of broader macroeconomic policy.16 For central banks, operational independence does not have to mean operational isolation. Rather, collaboration with government can be done in a way that builds and reinforces the social licence to operate, by showing a willingness to work with other partners to do whatever is necessary to achieve the broader objective—improving public wellbeing.

Even with coordination between monetary and fiscal policy, if further macroeconomic stimulus is needed quickly, the first line of defence will still inevitably fall upon central banks.17

In New Zealand, we are in the strong position of having further room to provide conventional monetary stimulus if required (using the OCR).

Having effective unconventional policy options expands the toolbox of a central bank, which is naturally more relevant in a low interest rate environment. In this spirit, we published a Bulletin article last year on the practicalities of unconventional monetary tools in a New Zealand context, and we continue to learn from the lessons of our central banking cousins.18

It’s better to have a tool and not need it, than need one and not have it.

Conclusion

In the Handbook, we explore the history of central banking objectives, and see how dramatically they have evolved over time. 19 We haven’t always had a mandate to support maximum sustainable employment, or to achieve price stability, or even control over interest rates or the money supply.

Nothing lasts forever, and it is possible that the role of central banks may change again in the future. Our Handbook will inevitably change. We need to be ready to adapt when changes beckon.

And it is not enough to grudgingly adapt. In order to maintain credibility, central banks must embrace change and prove to the public that they are capable of delivering on their objectives. To remain credible is to remain relevant. Central banks should keep their eyes open, and be ready to change tack. Our destination—a world with improved wellbeing for our citizens—may not change, but the best route for getting there may.

We must adapt. We must continue to improve the wellbeing of our citizens. We must remain credible.

Meitaki.

Thank you.

References

Blinder, A. (2006). Monetary policy by committee: why and how. DNB Working Paper No 92.

Drought, S., Perry, R., & Richardson, A. (2018). Aspects of implementing unconventional monetary policy in New Zealand. Reserve Bank of New Zealand Bulletin, 81(4).

Eichengreen, B. (2019, May 13). The Return of Fiscal Policy. Project Syndicate. Retrieved from https://www.project-syndicate.org/commentary/return-of-fiscal-policy-by-barry-eichengreen-2019-05.

Gerlach-Kristen, P. (2003). Monetary policy committees and the benefits of deliberation. University of Basel.

Grimes, A., Oxley L. and N. Tarrant (2012) Does Money Buy Me Love? Testing Alternative Measures of National Wellbeing. Motu Working Paper 12–09.

Irwin, N. (2014, December 19). Of Kiwis and Currencies: How a 2% Inflation Target Became Global Economic Gospel. New York Times.

Jacob, P. and A. Wadsworth (2018), Estimated policy rules for different monetary regimes: Flexible inflation targeting versus a dual mandate, Reserve Bank of New Zealand Analytical Note AN2018/11.

McDermott, J. and R. Williams (2018). Inflation targeting in New Zealand: An experience in evolution. Speech delivered to the Reserve Bank of Australia conference on central bank frameworks, in Sydney 12 April 2018.

Orr, A., & Aziz, O. (2019, March 29). In Service to Society: New Zealand's revised monetary framework and the imperative for institutional change. Retrieved from https://www.rbnz.govt.nz/research-and-publications/speeches/2019/speech2019-03-29.

Romer, D. (2011). What Have We Learned about Fiscal Policy from the Crisis? IMF Conference on Macro and Growth Policies in the Wake of the Crisis.

Sibert, A. (2005). Is the structure of the ECB adequate to the new challenge? Challenges for Central Banks in an Enlarged EMU, 97-117.

Svensson, L. E. (2014). How to Weigh Unemployment Relative to Inflation in Monetary Policy? Journal of Money, Credit and Banking, 46(S2), 183-188.

Wadsworth, A., & Price, G. (Forthcoming). Effective Monetary Policy Committee Deliberation in New Zealand. Reserve Bank of New Zealand Bulletin article.

Williams, R., Aziz, O., Kendall, R., Price, G., Ratcliffe, J., Richardson, A.,Wadsworth, A. (2019). Monetary Policy Handbook.

Appendix - Extracts from the May Monetary Policy Statement

Press Release

Tena koutou katoa, welcome all.

The Official Cash Rate (OCR) has been reduced to 1.5 percent.

The Monetary Policy Committee decided a lower OCR is necessary to support the outlook for employment and inflation consistent with its policy remit.

Global economic growth has slowed since mid-2018, easing demand for New Zealand’s goods and services. This lower global growth has prompted foreign central banks to ease their monetary policy stances, supporting growth prospects.

However, there is uncertainty about the global economic outlook. Trade concerns remain, while some other indicators suggest trading-partner growth is stabilising.

Domestic growth slowed from the second half of 2018. Reduced population growth through lower net immigration, and continuing house price softness in some areas, has tempered the growth in household spending. Ongoing low business sentiment, tighter profit margins, and competition for resources has restrained investment.

Employment is near its maximum sustainable level. However, the outlook for employment growth is more subdued and capacity pressure is expected to ease slightly in 2019. Consequently, inflationary pressure is projected to rise only slowly.

Given this employment and inflation outlook, a lower OCR now is most consistent with achieving our objectives and provides a more balanced outlook for interest rates.

Meitaki, thanks.

Summary Record of Meeting

The Monetary Policy Committee agreed on the economic projections outlined in the May 2019 Statement in order to provide a sound basis on which to form its OCR decision.

The Committee noted that inflation is currently slightly below the mid-point of the inflation target, and that employment is broadly at the targeted maximum sustainable level. However, the members agreed that given the recent weaker domestic spending, and projected ongoing growth and employment headwinds, there was a need for further monetary stimulus to meet its objectives.

The Committee agreed that the risks to achieving its consumer price inflation and maximum sustainable employment objectives were broadly balanced around the projection. Possible alternative outcomes were noted on the upside and downside.

A key downside risk relating to the growth projections was a larger than anticipated slowdown in global economic growth, particularly in China and Australia, New Zealand's largest trading partners. The Committee agreed that the projections adequately captured the observed global slowdown and its impact on domestic employment and inflation.

The Committee noted that additional stimulus from central banks had underpinned growth and reduced the likelihood of a more-pronounced slowdown. With some indicators of global growth improving in recent months, a faster recovery in global growth was possible. However, on balance, the Committee was more concerned about a continued slowdown rather than a faster recovery.

The Committee discussed other potential risks to domestic spending. The members acknowledged the importance of additional spending from households, businesses, and the government, to meet their inflation and employment targets. However, they noted several important uncertainties.

The Committee noted upside and downside risks to the investment outlook. Capacity pressure could see investment increase faster than assumed. On the downside, if sentiment remained low as profitability remains squeezed, investment might not increase as anticipated over the medium term. It was also noted that firms' ability to invest is constrained by the current competition for resources.

A potential source of additional demand discussed by the Committee included government spending being higher than currently projected, in view of the current strength of the Crown balance sheet. This view was balanced by the impact of any increase in government investment being delayed, for example due to timing of the implementation of new initiatives and current capacity constraints in the construction sector. The implications for monetary policy remain to be seen.

Some members noted that with lower mortgage rates and easing of loan-to-value requirements, any possible pick-up in the housing market could support household spending growth more than anticipated. The Committee noted that employment is currently near its maximum sustainable level. However, it was agreed that the outlook for employment growth is more subdued and capacity pressure is expected to ease slightly in 2019.

The Committee agreed that overall risks to the inflation projection were balanced. The Committee noted the outlook for inflation is below the target mid-point for longer than projected in the February Statement.

The recent period of rising domestic inflation was discussed. The Committee noted that the near-term outlook was more subdued due to lower capacity pressure. It was also noted that cost pressures remain elevated, and that there is a risk firms may pass these costs on as higher consumer prices by more than assumed. However, it was agreed that inflation expectations remain well anchored at the mid-point of the target range.

The Committee also noted the relatively subdued private sector wage growth, despite businesses suggesting that the inability to find labour is a significant constraint on their growth. The Committee noted the limited pass-through of the nominal wage growth to consumer price inflation.

Some members noted slower global growth reducing imported inflation was a downside risk to the inflation outlook.

The Committee reached a consensus that, relative to the February Statement, a lower path for the OCR over the projection period was appropriate. The lower path reflected the economic projections and the balance of risks discussed, and is consistent with both inflation and employment remaining near the Committee's objectives.

After discussing the relative benefits of holding the OCR and committing to a downward bias, versus cutting the OCR now so as to establish a more balanced outlook for interest rates, the Committee reached a consensus to cut the OCR to 1.50 percent.

Attendees

Reserve Bank staff: Adrian Orr, Geoff Bascand, Christian Hawkesby, Yuong Ha

External: Bob Buckle, Peter Harris

Observer: Gabriel Makhlouf

Secretary: Chris McDonald

Apologies: Caroline Saunders

Footnotes

1 Orr, A. (2019), In service to society: New Zealand’s revised monetary framework and the imperative for institutional change.

2 Irwin, N., Of Kiwis and Currencies: How a 2% Inflation Target Became Global Economic Gospel, New York Times, Dec. 19, 2014.

3 McDermott, J. and R. Williams (2018), Inflation targeting in New Zealand: An experience in evolution.

4 See also Jacob, P. and A. Wadsworth (2018).

5 Inflation data: NZ: Consumer Price Index (CPI) excl. food & energy; UK: CPI excl. food & energy; AUS: Trimmed mean CPI; USA: Personal Consumption Expenditure (PCE) excl. food & energy.

6 Grimes, Oxley, and Tarrant (2012).

7 The Handbook explains everything the public needs to know about making a monetary policy decision, and is available at: Monetary Policy Handbook page.

8 Chapter two of the Handbook.

9 See Blinder (2006), Gerlach-Kirsten (2006), Maier (2010), and Sibert (2005).

10 Chapter three of the Handbook.

11 Consensus-based decision making is requested in section 1b of the charter, available:

MPC charter April 2019 PDF 2MB

12 One of the specific tools we use are surveys of staff and MPC opinions on the balance of risks in the forecasts. This indicates both collective opinion, and quantifies the results. This greatly enhances the productivity of the MPC, as they don’t have to spend time discussing everything if they are already in agreement, and those who disagree with the majority can speak up and explain their position.

13 We don’t attribute the views to particular members. This can add noise to the summary, with the attribution distracting readers from appreciating the substance of the material.

14 Chapter seven of the Handbook describes the Reserve Bank’s approach to monetary policy strategy.

15 Svensson (2014) suggests that central banks should take a balanced approach to inflation and employment objectives. If you can’t keep both objectives at target at the same time, you should aim to have inflation and employment gaps with opposite signs. i.e., slightly undershooting on one metric, and slightly overshooting with the other. If you try to keep one objective at target with a gap in the other, it signifies that you are prioritising one of the objectives over the other.

16 For a recent and accessible read, see Eichengreen (2019).

17 Monetary policy can be adjusted more rapidly than fiscal policy, and have some immediate effects on financial conditions during a crisis (Romer, 2011).

18 Drought, Perry, & Richardson, 2018

19 Chapter four of the Handbook.