A speech delivered to Chartered Accountants Australia and New Zealand (CAANZ) in Auckland

1. Introduction

Kia ora koutou katoa

Last week, we unveiled a colourful new analogy to help tell the story of the Reserve Bank of New Zealand and the important work that it does to nurture the financial system and contribute to a well-functioning economy.

In this analogy, the Reserve Bank (or Te Pūtea Matua) is the big tree (Tāne Mahuta) that sits at the centre of New Zealand’s financial ecosystem. In Māori legend, Tāne Mahuta – the god of the forest and birds – separated Papatūāanuku (earth mother) and Ranginui (sky father) to let the sun shine and life flourish in Tāne’s garden.

In our context, Tāne Mahuta is the various elements that work together to deliver a sound and efficient financial system, and Tāne Mahuta’s garden represents the wider economy. Tāne’s roots are its legislation. Tāne’s trunk is the payment and settlement systems that allows the sap (or money) to flow throughout the system. The branches are regulated financial institutions, like banks, grafted onto Tāne for their legitimacy and lifeblood – access to money. The people working at the Reserve Bank are Tāne’s kaitiaki (its caretakers).

Today I’d like to talk about the important work that the Reserve Bank’s arborists do to take care of Tāne’s branches. That’s the Prudential Supervision Department that oversees regulated financial institutions to promote a sound and efficient financial system. Under our long-standing analogy, the Reserve Bank takes a ‘three pillar’ approach to prudential supervision. The pillars are: regulatory discipline, self-discipline and market discipline. In our new story we could think of these elements as the tools that Tāne’s arborists use in their work to promote a sound and efficient financial system.

Regulatory discipline involves setting rules and requirements. Self-discipline is aimed at supporting internal risk management and governance systems. Market discipline is the influence that investors and other stakeholders can have on an institution’s behaviour and risk profile. This needs user-friendly, authoritative and reliable information. Public disclosures supports the ability of investors and other stakeholders to exert market discipline.

Earlier this year, Deputy Governor Geoff Bascand discussed public disclosures and market discipline (Bascand, 2018). He also outlined a ground-breaking Reserve Bank initiative to enhance public disclosures by New Zealand incorporated banks called the Bank Financial Strength Dashboard. It’s a powerful new tool to help people make well informed decisions when putting their money in a bank. The Dashboard went live on 29 May with the firstquarter of data and was updated with additional data on 24 August.

I’ll outline how the Dashboard has been received, the role we all have to play to make disclosures effective and the Reserve Bank’s commitment to continue to improve the Dashboard. On this note, I am very pleased to announce that we are starting work on a te reo Māori version of the Dashboard. This initiative fits well with our strategic priority to promote understanding and trust through enhanced dialogue with stakeholders. The te reo Dashboard is another ambitious piece of work and it will take some time to get right but we are excited to start the journey.

2. What are prudential disclosures and why are they important

There has been a plethora of recent articles about the 10-year anniversary of the Global Financial Crisis (GFC). New Zealand came through that defining moment better than many countries. Our financial system was, and in my view still is, in good shape. Banks are well-capitalised and meet key regulatory requirements. In comparison to ten years ago, they are far less dependent on volatile short-term funding.

But one can never be complacent. The GFC smacked the world hard and, for many people, with minimal warning. As a Central Bank, we know it pays to be prepared. A key advantage of comprehensive, user-friendly disclosure is that it enables scrutiny of banks’ risks and financials by a wide range of stakeholders with different interests and perspectives (rating agencies, journalists, financial advisers, banks themselves and so on). It is why we are so passionate about it and why getting it right matters.

What are public disclosures? Banks are required to publicly disclose information about their business, the risks that they are taking and their financial resilience. This includes their financial statements as well as other information specifically about their risk and resilience such as credit ratings, capital adequacy, liquidity and the concentration of lending. Banks prepare these disclosure statements and make them available on their website. The Dashboard is basically a new way of presenting disclosure information in one place, and in a way that allows people to compare the information across banks. It complements the disclosure statements that banks will continue to prepare semi-annually.

In the hope of not overstating the Tāne Mahuta analogy, disclosures could be thought of as a spot light or perhaps a spyglass that Tāne’s arborists (Prudential Supervision) provide for New Zealanders so they can help keep an eye on the health of Tāne’s branches (which are the regulated entities like banks).

Why are public disclosures required?

The basic reason for imposing disclosure requirements is to better align the interests of banks with their customers and the wider community. In the absence of disclosures, there is a lack of transparency on how banks run their business and this may create incentives for bank managers to take risks that adversely affect the wider community. If left unchecked, banks may take excessive risks, which in an extreme scenario could threaten the stability of the financial system. So ultimately, the rationale for public disclosures is to help promote financial stability by increasing the transparency of how banks run their business and the risks they take.

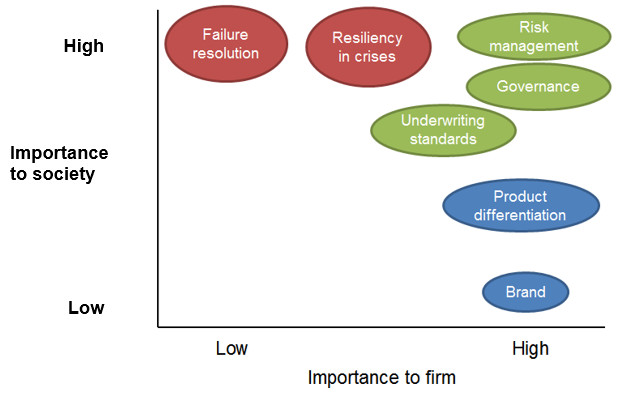

Figure 1: Selected interests of society and financial institutions

Referring to Figure 1, disclosure can increase bank resilience, by more closely aligning the firm’s incentives with society’s wider interests. By shedding light on metrics that indicate a bank’s risks and resilience, disclosure encourages its directors and management to improve their performance in these areas.

However, simply compelling banks to disclose information will not necessarily guarantee a good outcome of itself. There are many ingredients needed to ensure that disclosures work. Many fall to the regulator and other stakeholders also share some responsibility for making sure disclosures work effectively. Banks are responsible for providing quality data and users are responsible for engaging with the data and engaging with the regulator about their needs. I will come back to this shared responsibility nature of disclosures shortly.

Public disclosures are a common feature in many countries and have always played a particularly important role here in New Zealand. Our three pillars model emphasises the role of the market discipline pillar. The absence of explicit depositor protection and limited on-site verification by bank supervisors create strong incentives for the wider community to scrutinise the behaviour of banks.

Public disclosures are an important tool and do not work in isolation. The Reserve Bank has other tools at its disposal, such as minimum requirements on capital and liquidity, which are mutually reinforcing and work together with disclosures to promote financial stability. The calibration of these tools changes somewhat from time to time to respond to changing circumstances. For instance, minimum regulatory requirements were strengthened in the wake of the GFC but the role of disclosures remains a prominent feature of prudential settings in New Zealand (Fiennes, 2016b).

In addition to stability, the Reserve Bank is concerned with the efficiency of the financial system. Financial stability provides the right conditions for financial system participants to have the confidence to take appropriate risks and innovate over time, which is how our stability focus supports the dynamic efficiency of the financial system (Fiennes, 2014). The Dashboard represents a major step up in the effectiveness of disclosures, which we believe provides some additional efficiency benefits – more on this in a moment.

3. Disclosures are a shared responsibility

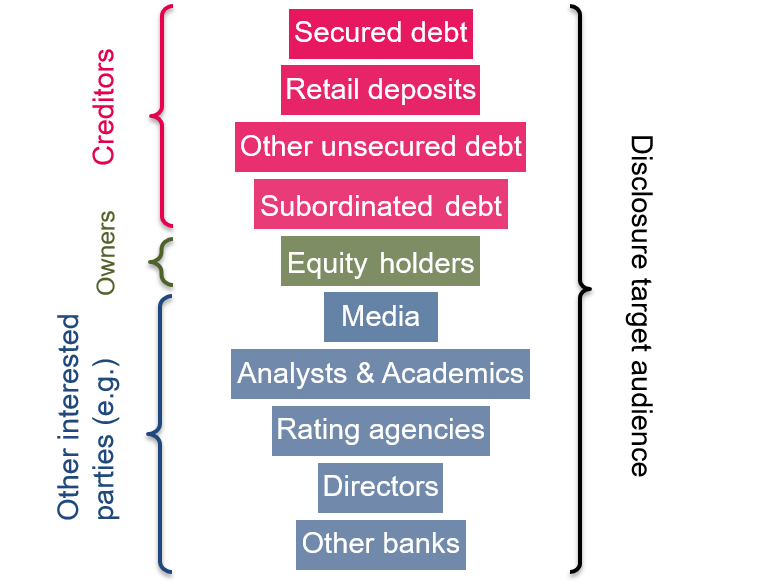

Getting disclosures right is a difficult task and everyone has a part to play. The regulator’s role is to establish a disclosure regime that meets the needs of a diverse group of users (see Figure 2). The international community has developed some best practice to help with this difficult task. For example, the Third Basel Accord has identified five principles of effective disclosures, which are that they must be: 1) clear; 2) comprehensive; 3) meaningful to users; 4) consistent over time, and 5) comparable. In addition to this list, the Reserve Bank believes that market participants must have incentives to monitor banks and mechanisms to exercise discipline, such as reasonable alternative investment options provided by a competitive marketplace (Fiennes, 2016). Another equally important element of effective disclosures is that stakeholders must have confidence in the information being disclosed (Bascand, 2018). Banks and users of disclosures also have a role to play. Banks are expected to provide quality data and users are responsible for engaging with the data and engaging with the regulator about their needs.

Figure 2: Target audience for prudential disclosures

Simply stating that good disclosures is a shared responsibility is of little value unless the appropriate tools and incentives are also in place. For banks, disclosures are a regulatory requirement but banks also benefit from disclosures because the information they provide is useful for benchmarking risks and performance. On this note, the Dashboard has been welcomed by a number of banks because they see benefits in getting easier access to better benchmark data. Some stakeholders, such as journalists and rating agencies, have fairly clear professional or business incentives to monitor disclosures. Bank creditors and owners also have quite clear incentives to monitor disclosures because they care about the safety of their money.

I should note at this point that we have seen genuine positive changes as a result of the launch of the Dashboard. For example, banks have improved the scrutiny they apply to their own liquidity metrics now that these are in the public domain. We have also seen commentator interest in some of the detail, such as rural exposure or concentration risk. Financial journalists have used Dashboard information to compare capital and liquidity ratios across the banking sector, and discuss their meaning. Independent rating agencies advise that they actively use the Dashboard in their assessments.

These are all positive and encouraging developments. Of course, we are always looking for ways to improve both the content and the use of the tool – I shall discuss this later.

This is a good opportunity to emphasise the trade-off between risks and return that is part of any investment decision. After all, placing money with banks is an investment decision that comes with risk, even if the risk is usually low. This is why there are clear and direct incentives for all creditors, including retail depositors, to take an interest in the financial condition of their bank and how they manage risks. And this is where prudential disclosures, like the Dashboard come in – they are intended to assist bank customers and their advisers to understand more about the financial condition of banks operating in New Zealand.

While creditors have vested interests in disclosures, the Reserve Bank recognises that engaging with certain creditors, like retail depositors, is a challenge because they are a large group of people with varying levels of financial literacy. For this reason, the Dashboard was developed with a strong focus on making prudential disclosures understandable and accessible for a general audience. This includes developing a series of explanatory videos, presenting the information in a layered format and an emphasis on using charts to help users draw insights from the data.

As Tāne Mahuta’s arborists, we recognise that tools like disclosures need to be regularly maintained in order to remain effective. The Dashboard is a good example of our ongoing work to adapt and maintain prudential disclosures.

4. Wider research into market discipline

We have also begun an initial exploration into how market discipline operates in our financial ecosystem. This study, to be released later in the year, will be the first of its kind for New Zealand and we hope to lay the foundations for further investigation of market discipline. Although not yet complete, our study does provide evidence that market discipline does indeed work to reduce financial risk in our garden but that there is room for improvement.

To this end we are working to improve the accessibility and comparability of disclosure information through initiatives such that the Dashboard. While it is always difficult to judge how useful a given tool is without a counterfactual there are a number of instances where disclosure of risk information has prompted a reaction from the markets. Chief among these is the disclosure of credit ratings. In our preliminary study of market discipline, we have found that changes in credit ratings have a tangible effect on a bank’s cost of funding. People do pay attention to developments in the market and react accordingly.

To this end we are working to improve the accessibility and comparability of disclosure information through initiatives such that the Dashboard. While it is always difficult to judge how useful a given tool is without a counterfactual there are a number of instances where disclosure of risk information has prompted a reaction from the markets. Chief among these is the disclosure of credit ratings. In our preliminary study of market discipline, we have found that changes in credit ratings have a tangible effect on a bank’s cost of funding. People do pay attention to developments in the market and react accordingly.

We believe the influence credit ratings have on people is partly owed to their accessibility, comparability and most importantly, the credibility of its publisher. In the development of the Dashboard we have striven to follow this example.

5. What is the Dashboard and how does it work

The Dashboard is an online and interactive central repository of disclosure data that is updated quarterly. It is a tool designed and developed by the Reserve Bank to enhance the effectiveness of prudential disclosures, boost market discipline and support the Reserve Bank’s financial stability and efficiency mandate. The Dashboard concept for disclosures was born out of a broad review of prudential regulatory settings in 2015 called the Regulatory Stocktake, where we identified stakeholder appetite for timelier, more accessible and more comparable prudential disclosures. The Dashboard concept was refined through public consultation, and engagement with industry, and launched in May 2018. There are now two quarters of data available on the Dashboard and this resource will become increasingly useful as the time series develop.

The Dashboard sits alongside disclosure statements as a source of meaningful information for interested users to better understand and compare a bank’s business and its risks. As a result of the Dashboard, the frequency of disclosure statement publications was reduced from quarterly to six-monthly. Annual and half-yearly disclosure statements remain useful for users and contain directors’ attestation statements.

The Dashboard data comes from private reporting that banks provide to the Reserve Bank whereas the disclosure data is prepared and published by banks themselves. As well as minimising compliance costs, using private data allows for better comparability across banks because the information on the Reserve Bank sets standard definitions – accounting standards, used for other disclosures, can allow for significant discretion. That said, banks have an incentive to achieve as much consistency as possible between the Dashboard and their disclosure statements so it is reasonable to expect banks to adjust their disclosure statements or provide reconciliations to minimize the impact of any remaining differences. It is worth noting that disclosure statements are subject to auditor scrutiny, whereas Dashboard data is not. This lack of auditor scrutiny is one factor that allows the Dashboard to be published up to 4 weeks sooner than annual disclosure statements.

6. Accommodating diverse users

The target audience for prudential disclosures is diverse and includes creditors, owners and other interested parties like the media, rating agencies and the banks themselves (see Figure 1). These users differ in a number of ways such as their financial literacy and preferences for different information presentation formats (ie raw data, written text and visualizations). It is reasonable to expect a large gap in financial literacy between some user groups, especially between the typical retail depositor and frequent users of disclosures like academics, financial journalists and professional investors. These types of difference were taken into account in the design and implementation of the Dashboard.

The starting point for the design of the Dashboard website was its predecessor, a little used data table (called the G1 table) prepared by the Reserve Bank and assembled from individual bank disclosure statements. A number of design iterations and some user experience testing revealed that a very graphics forward design, along with plain English explanatory materials and education videos were needed to adequately accommodate the range of expected Dashboard users. The Reserve Bank reached out to other government agencies and financial journalists to help the development of understandable explanatory materials and educational videos. The Dashboard contains a number of interactive features that are all intended to help users to compare banks side by side on key metrics.

Importantly, the layered design and the various interactive features on the Dashboard will, over time, provide a rich source of information on the demand for and use of prudential disclosures going forward. This information could shed light on how market discipline operates in New Zealand and provide useful guidance on how to further enhance prudential disclosures.

In designing the Dashboard, we had to make a number of trade-offs. In particular, whenever one thinks about a data availability over time (time series’ continuity), one has to consider whether to keep the old series and add to it, or accept a break in the data. In the case of the Dashboard, we took two key decisions:

- Standardising definitions brings clear benefits of comparability across banks and over time. It does, though, mean a break in some time series now no longer available more than half-yearly because they are not included in the quarterly Dashboard;

- We preferred to get it right. While the series provided on the Dashboard are standardised and comparable across all banks a few do not fully match all of the series provided by banks in their individual disclosure statements due to the discretions banks have. Where new harmonised series were introduced a long run time series will evolve over time.

7. Who is using the Dashboard

The Dashboard was launched on 29 May with a dedicated promotion. It was featured in the May Financial Stability Report (FSR). A 2-week online and digital media campaign supported the launch with a follow-up burst in August. We received a lot of positive feedback on the ease of use of the Dashboard from many sources including financial journalists, academics, and a number of government agencies.

Early usage statistics were positive. The Dashboard received more visits in its first 24 hours than its predecessor (the G1 table) typically receives in an entire year. The vast majority of these visits are from New Zealanders. An interesting observation is that about 15% of users to date are return visitors, which is an indication that a number of users view the Dashboard as a resource rather than just a one-off curiosity.

An important question is whether we have succeeded in reaching a broader audience for disclosures with the Dashboard. The early usage statistics we have seen are encouraging but a better picture of the Dashboard’s impact will emerge over time as awareness builds and the data becomes more valuable by showing trends.

Other stakeholders like financial journalists play a role in building awareness and understanding of prudential disclosures. One example is the online publication Interest.co.nz who featured the Dashboard data on their website.

Feedback from users suggests they appreciate the accessibility and better quality of information the Dashboard contains compared to the previous G1 table and off-quarter disclosure statements.

We are aware that simply publishing the Dashboard will not be enough to engage all the user groupings we want to reach. This is why we will be proactively seeking engagements with all of these groups. Efforts to enhance financial literacy and further accessibility will continue. A te reo Māori version of the Dashboard, perhaps in a year’s time, should be seen in this context.

At the other end of the spectrum, we have had good engagement from “superusers” – academics, rating agencies, specialist financial journalists. Some have asked for less static data, and for us to introduce scenario analysis. For example, stress test results may contain useful information for the riskiness of individual banks. We plan to review the case for making individual bank results publically available alongside the next stress test, building on the steps we have already taken to increase the granularity of stress test reporting (Lilly, 2018).

8. What are the expected benefits of the Dashboard

There are a number of benefits (see Figure 3). First and foremost, better disclosures as a result of the Dashboard are expected to enhance market discipline, which in turn provides a financial stability benefit. Other benefits include better benchmark data, better quality disclosure data and insights into the use of disclosure data.

The Dashboard makes a significant contribution to efficiency by providing better data to markets and reducing the costs for users to use disclosure data. Better information can help financial market allocate funding to their best use, which is what we call allocative efficiency. It also contributes to dynamic efficiency by making life easier for a lot of users and supporting financial stability (a necessary condition for innovation). Presenting Dashboard data alongside information on returns (for example interest rates on term deposits at the bank) makes the risk reward trade-off more apparent.

Figure 3: Expect Dashboard benefits

9. We are committed to meeting user needs for prudential disclosures

The Dashboard is innovative for a number of reasons including that it is the Reserve Bank’s first native cloud application, which means that it lives in the cloud (Amazon Web Services to be precise). And we have already noted how the Dashboard represents a big improvement of the regulatory process of disclosures, especially for users. We consider the Dashboard an example of regulatory technology (or RegTech) because it uses information technology to enhance the regulatory process of disclosures.

The Reserve Bank is committed to further developing the Dashboard disclosure tool to reflect the evolving needs of users, changes in domestic regulatory policy settings and updates to international best practice. This commitment includes doing more work to educate users. For example, by contributing to efforts to boost the financial capability of New Zealanders. In other words, as Tāne Mahuta’s arborist, we are committed to ensuring that we have the right tools in place to look after Tāne’s branches, which includes the banks.

In terms of the Dashboard tool itself, there is a short list of developments underway. The most immediate of these is the development of a public Application Programme Interface (API) to allow more flexible and efficient use of disclosure data. The public API will be particularly useful for users who want to make regular use of disclosure data for analytical or reporting purposes, and to mash it with other data from different sources, such as rates of return or other non-financial disclosures such as customer satisfaction metrics. Over time trend information will be available as data accumulates.

A challenge I want to throw to the banks themselves, to their customers and to commentators is to tell us what else you want to see in the Dashboard and how this can be presented.

It is arguable that society now expects more than compliance with the bare regulatory minimum. To be clear, we have no ability to take action against regulated entities that operate above regulatory minima and nor should we. But we may have a role in facilitating disclosure: for example in the wake of the recent Australian Financial Services Royal Commission’s interim report, there is much focus on misconduct and fair treatment of customers. We would welcome ideas on whether there are “conduct” metrics that could and should be included. The same question arises in the context of operational risk, such as business continuity arrangements. What, for example, would be a minimum or standard benchmark and how should one define and source the information?

These ideas, along with that of presenting stress test results (see above), are qualitatively different from the current role of the Dashboard, which is to present well-understood, consistently-defined information in a single place. That is why it is both exciting and challenging to be thinking about the next stage of evolution of a tool that has, in a few short months already exceeded my high expectations. I welcome ideas – bring them on!

Finally, the Reserve Bank is keen to explore disclosure dashboards for other sectors like insurance and non-bank deposit takers. Insurance is likely to be the next cab off the rank and we expect to start work in earnest in mid-2019, once we have a good sense of how the bank Dashboard has worked. We are excited about this, seeing an insurance dashboard as a great opportunity to further improve transparency of the sector and of our supervision of insurers.

10. Conclusion

We have covered a lot of ground in our Journey around Tāne Mahuta’s garden today. Hopefully our new analogy helps you to better understand what we as Tāne’s arborists (Prudential Supervision) do with tools like disclosures to help promote a sound and efficient financial ecosystem.

The Dashboard is a new and improved disclosure tool that represents an important step forward in meeting the needs of our diverse user community for timely, comparable and accessible information on the financial and prudential condition of New Zealand incorporated banks. Our focus on meeting user needs reflects the fact that we all have a role to play to make disclosures effective. Banks provide quality information. Users, including the general public, engage with the Dashboard and let us know what needs further improvement. As Tāne’s arborists we are responsible for making sure that tools like the Dashboard are up to the task and upgraded when needed. On this note, we are committed to further improving the Dashboard to meet user needs. This includes making improvements to the Dashboard itself and working to help build the capability of New Zealanders to understand and make use of the Dashboard.

Our plans for a te reo version of the Dashboard is an exciting initiative that fits our strategic priority to build trust and enhance dialogue with our stakeholders.

Tēnā koutou katoa

View the Bank Financial Strength Dashboard

Read the article: The Journey of Te Pūtea Matua: our Tāne Mahuta

The Reserve Bank would like to thank Northern hapu Te Roroa, who act as kaitiaki (guardian) to Tāne Mahuta, for their support of our Tāne Mahuta narrative.

References

- Bascand, G (2018). The effect of daylight: disclosure and market discipline. A speech delivered to the NZ Bankers’ Association, 28 February.

- Basel Committee on Banking Supervision (2015). Revised Pillar 3 disclosure requirements. Bank for International Settlements Standards.

- Bloor, C., Hunt, C (2011). Understanding financial system efficiency in New Zealand. Reserve Bank Bulletin, Vol 74 No. 2.

- Fiennes, T. (2016a). Regulation and the importance of market discipline. A speech delivered to the NZ Bankers Association and Bank of New Zealand, 4 February.

- Fiennes, T. (2016b). New Zealand’s evolving approach to prudential supervision. A speech delivered to the NZ Bankers’ Association, 01 September.

- Fiennes, T. (2014). The risk management quest: a Reserve Bank approach. A speech delivered to the NZ Society of Risk Management, 01 September.

- Lilly, C. (2018) ‘Outcomes from the 2017 stress test of major banks’, Reserve Bank of New Zealand Bulletin, Vol. 81, No. 8, June 2018.

- O’Connor-Close, C., Austin, Neroli (2016). The importance of market discipline in the Reserve Bank’s prudential regime. Reserve Bank Bulletin, Vol 79 No. 2.