A speech delivered to the Manawatu Chamber of Commerce in Palmerston North

Introduction

Thank you for the opportunity to meet with you this afternoon.

My comments today will focus on the process of making a monetary policy decision. I do not intend to send any particular messages about upcoming monetary policy announcements.

Seven times a year, the Bank announces a decision to set the Official Cash Rate (OCR). Four of these announcements are accompanied by a Monetary Policy Statement.

Each OCR decision and Statement publication is a complex process involving many staff from across the Bank. The significant amount of background work reflects the uncertainty we face when setting monetary policy to achieve the objectives of the Policy Targets Agreement (PTA).

As one example of this uncertainty, major economic data are often released with a significant lag, and remain subject to revision for some time. This makes interpreting even the current economic environment difficult.

Inflation-targeting central banks have adopted some common features in their decision making to deal with uncertainty. These include policy discussions within a committee environment, consideration of a wide set of information, a focus on transparency and clear communication to stakeholders, and generally modest moves in policy settings with the chance for regular review.

Today I want to focus on the Bank’s approach to two of these elements – committee decision making and reviewing our forecasts. My comments summarise some recent and upcoming Bulletin articles.1

Making a monetary policy decision

The Bank has used committees in its monetary policy decision making process for many years. Historically, their use has been most prevalent in policy discussion and advice.2 In 2013, the Bank maintained the advisory role of its committees, and strengthened the role of committees in making a monetary policy decision.3

These changes mean the Bank now relies less on the single decision maker model. The Governing Committee was formed, with this committee responsible for reaching a decision on the appropriate setting for monetary policy. The Governing Committee consists of the Governor, the Deputy Governors and the Assistant Governor. The Governor retains statutory responsibility for policy decisions.

The Governor’s decision making responsibility is similar to the arrangement at the Bank of Canada, which has a single decision maker model in its legislation, but makes policy decisions within a committee framework. Making a decision by committee allows the consideration of a greater range of viewpoints. A group of individuals with a diverse and differing set of useful information should make generally more informed decisions than an individual.4

The Bank’s Monetary Policy Committee (MPC) acts as an advisor to the Governing Committee on monetary policy issues. The MPC is made up of several senior staff (including the Governors) and two external advisors.

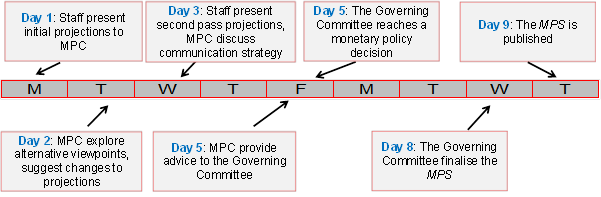

After extensive background analysis, members of the Bank’s staff, the MPC and the Governing Committee work together over a 9-day period towards making a monetary policy decision and publishing a Statement (figure 1).

In the first three days of this process, the Governing Committee has discussed with the staff and MPC: current economic and market developments; an initial set of economic projections; key risks and judgements that make up the projections; and a number of alternative scenarios and policy options. This is supplemented by a range of additional information relevant to the policy outlook, including information on trends in household and business credit and unobservable variables like the output gap, inflation expectations and the neutral interest rate. Particular effort has been made over these three days to ensure a diverse range of views and opinions have been heard.5 The set of meetings conclude with a final set of conditional projections for the economy over the next 2-3 years and a conditional projection for the 90-day bank bill rate.

Figure 1: The monetary policy decision making process in New Zealand

After consideration of this information, the Governing committee meet on day five of this process to reach a broad range of decisions on monetary policy. The meeting has a number of goals. One aspect of the decision-making process is to reach a decision on the OCR. This decision is often the one that gains the most public focus.

However it is not just today’s OCR, but the full outlook for interest rates, which is important for influencing today’s consumer and business behaviour and ultimately inflation. As a result, the Governing Committee also puts significant focus in its deliberations on reaching a consensus on the outlook for interest rates consistent with the objectives of the PTA. The Governing Committee also works towards a consensus on what key messages to include in the Statement.

The meeting begins with the Governor summarising the written advice of the MPC (including members of the Governing Committee). The Governors then discuss the MPC advice, their own views, and points of difference. If there are competing viewpoints within the Governing Committee, the members have an opportunity to reconsider their positions. Once the Governing Committee has reached a consensus on the range of policy considerations the Governor then formalises the decision

The Governing Committee is a collegial committee, in that it aims to reach consensus on appropriate policy settings through debate. The collegial approach is advantageous in that is helps the Bank to sharpen the communication of a policy decision.

If the Governing Committee is unable to reach a consensus view on the range of policy considerations, it will go with the majority view if one exists. If the views are balanced, the Governor will have final say on the policy outcome. Once a decision has been finalised, each member of the committee adopts the outcome as their own position when speaking in public, ensuring a consistent message and unified voice.

Reviewing our performance

Making a decision in a committee setting is one way the Bank deals with the uncertainty faced in setting policy. Another way to deal with this uncertainty is to regularly review our policy decisions and framework. This helps the Bank improve its state of knowledge of the economy and learn from any past errors.

A number of reviews have been conducted on the elements of the Bank’s monetary policy framework. These include formal reviews, like in 2001 and 2007.6 In addition, the Bank often invites other central bank and academic economists to observe the decision-making process and provide comments on potential areas of improvement.7 A recent study by the BIS indicated that the Bank has self-commissioned more reviews than any other central bank.8

One further avenue of review is to assess our own forecasting performance.9 Reviews of forecast performance help to update our understanding of economic relationships, evaluate risks to the current outlook and identify areas where we could improve our accuracy.

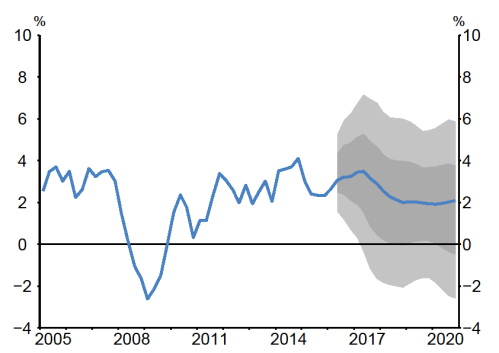

The Bank will always make forecast errors, reflecting the uncertainties in assessing the current state of the economy and its outlook. For example, the vast majority of forecasters were unlikely to have been able to accurately predict the sharp decline in oil and export commodity prices that occurred over 2014 and 2015 – one factor that has led to current low inflation. To further illustrate the point, figure 2 shows the Bank’s central outlook for annual GDP growth and the error bands around this estimate implied by our past forecast errors.

Figure 2: June Statement annual GDP growth forecast and error bands

Note: The error bands displayed above reflect the direction and magnitude of the Bank’s past annual GDP growth forecast errors at different forecast horizons, calculated over the period 2010q1-2016q1. To set the range of the error bands, the Bank’s forecast (in blue) is adjusted for bias using the Bank’s mean forecast error at each relevant horizon. The error bands are then set symmetrically relative to this bias adjusted forecast, using the standard deviation of the Bank’s past forecast errors at each relevant horizon. The dark shaded areas cover +/- one standard deviation. The light shaded areas cover an additional +/- one standard deviation.

To say the potential for forecast errors is large is an understatement. So why do we even forecast at all? There are two important reasons. First, monetary policy influences activity, including wage- and price-setting behaviour, with a lag. Second, it is the outlook for the economy that matters for the economic behaviour of firms and households today. Therefore, we need an understanding of the likely direction of the economy over the next few years, to guide our monetary policy strategy to achieve price stability.

We do a number of things to deal specifically with the uncertainty of our forecasts. First of all, we use a range of additional information to supplement our projections and guide our policy decisions, rather than relying solely on model driven forecasts. This includes market intelligence from our business liaison programme and the 120 or so presentations we make around the country to business and other groups each year.

Second, we aim to highlight the conditional nature of our forecasts, and how we would respond if conditions developed differently. That way, financial market participants can anticipate our likely response when the economy evolves in an unexpected way. This helps to shift the yield curve towards levels consistent with medium-term price stability without the constant need for comment from the Bank. The Bank’s approach to forward guidance is something I talked about in a speech earlier in the year.10

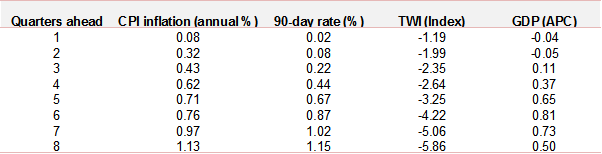

Third, we regularly investigate what we can learn from our past judgements. Table 1 presents the Bank’s forecast errors on key macroeconomic variables since the first quarter of 2010. The Bank’s projections have been inaccurate in two specific respects over this period. CPI inflation has been consistently weaker than forecast, while the New Zealand dollar has been stronger than forecast.

Table 1: Mean forecast error (Monetary Policy Statement forecasts)

Note: This table presents the mean errors of the forecasts from the Bank’s Statement made over the period 2010q1 to 2016q1. CPI inflation, 90-day rate and GDP errors are in percentage points and the TWI errors are index points. A positive number implies the outturns were lower than the Bank had forecast.

One way to assess what we can learn from forecast errors is to benchmark our performance against other forecasts. Lees (2016) and Reid (2016) benchmark the Bank’s forecasting performance against other forecasters and the Bank’s own statistical models respectively. If the Bank’s forecasts are significantly less accurate than other forecasters or our own statistical models, then we can likely gain insights from these sources to improve our own modelling and forecasting framework.

Generally, the Bank’s recent forecasts have performed well relative to these benchmarks. Looking at the period since the financial crisis, the Bank has been one of the better forecasters of New Zealand macroeconomic variables. In addition, the Bank’s forecasts are of a similar quality to those produced by our suite of statistical models. Overall, the Bank, other forecasters and the Bank’s statistical models did not foresee the persistent weakness in inflation or the persistent strength in the New Zealand dollar. This is a reflection of the inherent uncertainty that analysts and policy makers have to deal with when forecasting the New Zealand economy.

Despite this, the persistent period of weaker-than-expected inflation remains a focus for the Bank. Low inflation has been a common experience in most advanced and many emerging economies. The Bank has shifted its resources in recent years towards more fully understanding this low inflation environment, and this is a strategic priority in the Bank’s 2016 Statement of Intent.

The Bank has completed a range of research topics that have shed some light on the drivers of low inflation. This includes an assessment of international influences (including the exchange rate),11 a review of our frameworks for estimating key unobservable variables,12 assessing the inflationary consequences of different migration drivers and strong labour supply growth,13 and highlighting the potential impact of adaptive inflation expectations on current inflation.14 The Bank will continue to update the public on the drivers of low inflation in speeches, research articles and the Statement.

Conclusion

Each OCR decision and Statement publication involves a lot of work from a number of staff around the Bank. This staff involvement reflects the inherent uncertainty the Bank is faced with when making a monetary policy decision. We have set up processes to help deal with this uncertainty and improve the quality of our monetary policy decisions.

For much of the Bank’s history, advisory committees have been a key element of this process. Since 2013, the Bank has given a greater role to committees in monetary policy decision making. The Governing Committee works together to reach a decision on the appropriate setting of the OCR and the key contents of the Statement.

A further important element of the Bank’s decision-making process is the opportunity for constant review. Since the financial crisis, inflation has persistently been weaker than forecast, and the Bank has continually reviewed its forecast performance over this period. Recent research has shown that the Bank’s forecast performance has been reasonable when compared to a number of benchmarks. This suggests that there were no obvious major sources of new information that the Bank could have used from these benchmarks in its decision making.

Even so, the persistent period of weaker-than-expected inflation remains a focus for the Bank, and the Bank’s research program is shedding light on the drivers of low inflation. Increasing our understanding of low inflation is a strategic priority for the Bank.

References

1 See: Lees (2016), ‘Assessing forecast performance’, Reserve Bank of New Zealand Bulletin, Vol. 79. No. 10. June 2016; Reid (forthcoming), ‘Evaluating the Reserve Bank’s forecasting performance’, Reserve Bank of New Zealand Bulletin; and Richardson (2016), ‘Behind the scenes of an OCR decision in New Zealand’ Reserve Bank of New Zealand Bulletin, Vol. 79. No. 11. July 2016.

2 For a description of previous approaches to decision making at the Bank see: Brash (2001), ‘Making monetary policy: a look behind the curtains’, remarks by Donald Brash, Governor of the Reserve Bank of New Zealand, 1 March 2001; RBNZ (2007), ‘Submission to the Finance and Expenditure Committee inquiry into the future monetary policy framework’

3 See Wheeler (2013), ‘Decision making in the Reserve Bank of New Zealand’, remarks by Graeme Wheeler, Governor of the Reserve Bank of New Zealand, 7 March 2013.

4 For a discussion of theory and evidence, see Blinder (2004), ‘The Quiet Revolution: Central Banking Goes Modern’, Yale University Press.

5 For a full description of this process see Richardson (2016).

6 See: RBNZ (2001). ‘The monetary policy decision-making process’, Independent review of the operation of monetary policy supporting paper; RBNZ (2007) above.

7 These visitors will often present a paper containing views on the decision making process and recommendations to improve the process.

8 BIS (2016), ‘Self-initiated reviews of the central bank’s policy performance’, background note for the February 2016 meeting of the Central Bank Governance Group.

9 Past forecast performance reviews include: McCaw S and Ranchhod S (2002), ‘The Reserve Bank’s forecasting performance’, Reserve Bank of New Zealand Bulletin, Vol.65, No.4; Turner J (2006), ‘An assessment of recent Reserve Bank forecasts’, Reserve Bank of New Zealand Bulletin, Vol.69, No.3; Labbe F and Pepper H (2009), ‘Assessing recent external forecasts’, Reserve Bank of New Zealand Bulletin, Vol.72, No.4.

10 McDermott (2016), ‘Forward guidance in New Zealand’, remarks by John McDermott, Assistant Governor of the Reserve Bank of New Zealand, 4 February 2016.

11 Richardson (2015), ‘Can global economic conditions explain low inflation in New Zealand’, Reserve Bank of New Zealand Analytical Note AN2015/03.

12 See: Richardson and Williams (2015), ‘Estimating New Zealand’s neutral interest rate’, Reserve Bank of New Zealand Analytical Note AN2015/05; Armstrong (2015), ‘The Reserve Bank of New Zealand’s output gap indicator suite and its real-time properties’, Reserve Bank of New Zealand Analytical Note AN2015/08; Lewis, McDermott and Richardson (2016), ‘Inflation expectations and the conduct of monetary policy in New Zealand’, Reserve Bank of New Zealand Bulletin, Vol. 79. No. 4. March 2016.

13 See: Armstrong and McDonald (2016), ‘Why the drivers of migration matter for the labour market’, Reserve Bank of New Zealand Analytical Note AN2016/02; Vehbi (2016), ‘The macroeconomic impact of the age composition of migration’, Reserve Bank of New Zealand Analytical Note AN2016/03.

14 See Karagedikli and McDermott (2016), ‘Inflation expectations and low inflation in New Zealand’, Reserve Bank of Discussion Paper Series 2016/09.