A profitable banking system is beneficial for financial stability, as it enables banks to generate or attract the capital base needed to absorb potential losses over economic cycles. At the same time, competition between banks has an important role in supporting an efficient, inclusive, and dynamic financial system. In light of this, this special topic analyses recent trends in bank profitability and compares key profitability indicators within the New Zealand banking sector and between banks in peer countries.

In nominal terms, profitability in the New Zealand banking sector fell materially in 2020, as banks increased provisioning for expected losses as a result of the COVID-19 pandemic (figure 2.7).

However, nominal profits recovered strongly over 2021 and 2022 alongside growth in the New Zealand economy. In particular, banks’ profits were aided by less impairment expenses than was initially expected and higher net interest margins (NIMs) (figure 2.8). 11

Several factors have contributed to the higher NIMs:

- Deposit growth has been strong, supported by the large monetary and fiscal stimulus introduced at the start of the pandemic. Deposits are a high quality source of funding for meeting banks’ core funding requirements, contributing to banks’ current strong funding positions (see Chapter 4). Lending growth has also been subdued in recent times. These conditions have reduced the need for banks to use more expensive wholesale funding and to compete for further deposit funding. This has kept deposit rates and, therefore, banks’ funding costs lower than otherwise.

- The lags in monetary policy transmission that mean higher interest rates are taking longer to pass through to banks’ funding costs. This means NIMs are temporarily higher than otherwise while the economy transitions to higher interest rates. As interest rates have risen considerably faster than they have in previous tightening cycles, this transitory effect has been more pronounced than in the past. In particular, these lags include the following:

- Rates on short-duration deposits, such as transaction and on-call savings accounts, have not increased as quickly as the Official Cash Rate (OCR) and the interest income banks earn on their assets (figure 2.9). Consequently, these deposits have become increasingly profitable sources of funding relative to term deposits or issuing debt in wholesale markets.

- Following heightened uncertainty and low interest rates during the pandemic, the proportion of banks’ deposit books in short-duration deposits was above its long-run average at the start of the tightening cycle. While savers are moving back to term deposits as interest rates rise, this transition is lagging the increase in interest rates (figure 2.10). Banks have been comfortable holding more short-duration liabilities than historically due to their strong liquidity positions, holding down their average funding costs.

The above factors mean banks have had relatively lower interest costs in the past 18 months, while lending rates and interest income have increased alongside the OCR, supporting a recovery in banks’ profits.

However, measuring profitability in nominal terms does not control for variables such as growth in the size of a business over time and inflation. Profitability ratios, such as the return on assets and return on equity, are more robust indicators of performance. Banks’ balance sheets have continued to grow since 2020, reflecting growth in the economy (figure 2.7). Their equity bases have been further supported by lower dividend payout ratios, as banks have started to increase capital in anticipation of the higher future capital requirements. As a result, the return on assets and return on equity are at similar levels to those in the decade prior to the pandemic (figure 2.11).

Download the graph showing profitability ratios (jpg, 264 KB)

While the banking sector as a whole does not appear to be materially more profitable in 2023 compared to the past 30 years, the large New Zealand banks have been more profitable than the rest of the New Zealand banking sector and large banks in a number of comparable economies in recent years (table 2.2).

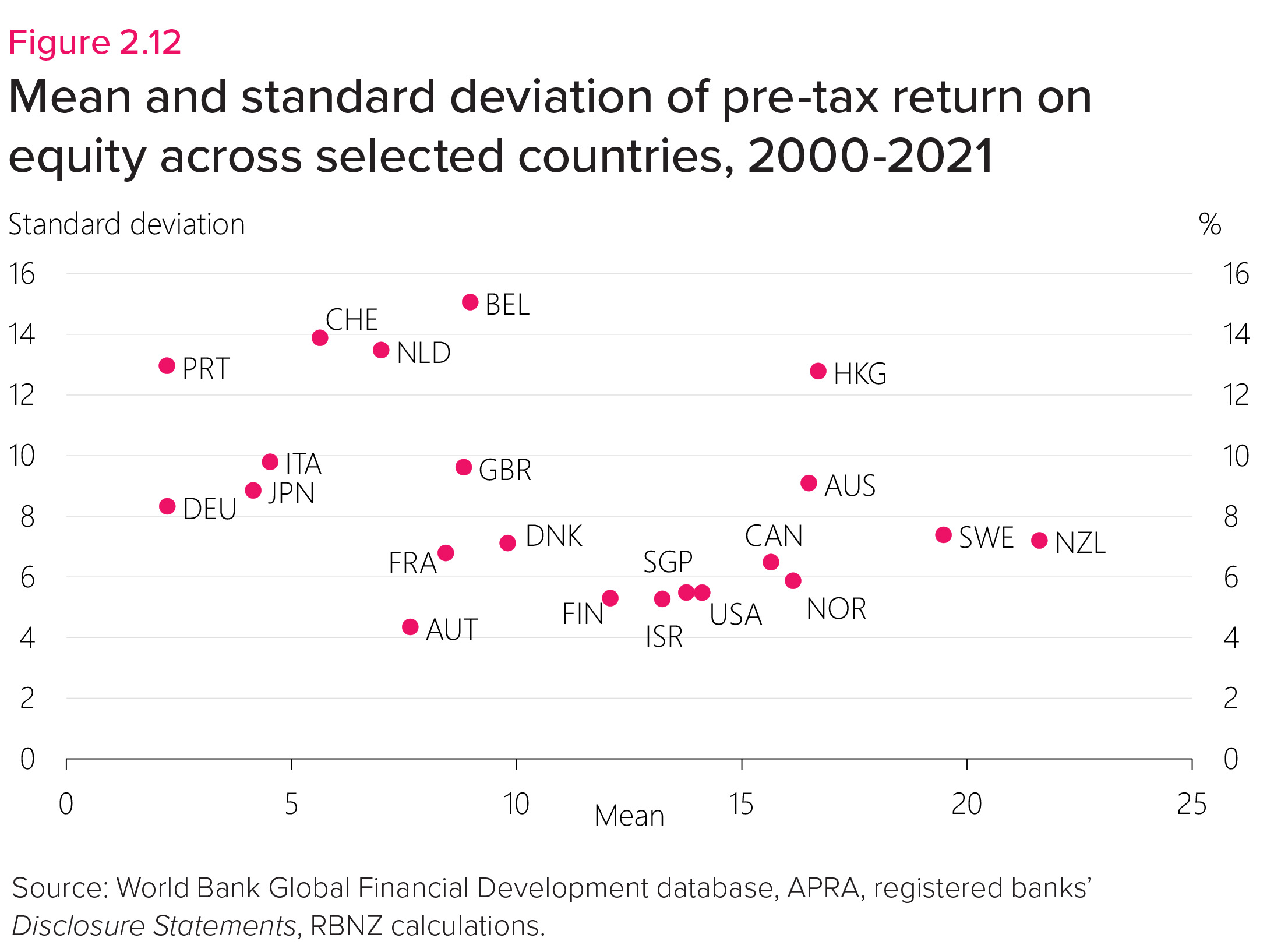

Higher risk associated with operating a bank in New Zealand relative to other countries is a potential driver of high profitability for New Zealand banks. However, the volatility of earnings, a standard measure of risk, has been relatively low in New Zealand compared to other countries in recent decades (figure 2.12). This suggests that risk does not fully explain the relatively higher returns of New Zealand banks, although it should be noted that this has been a period of ongoing economic growth and strong housing market performance.

The differences in risk-adjusted profitability may reflect a lack of competition. However, several other drivers are possible:

{kind=link}

{kind=link}

- The revenues of New Zealand banks relative to the size of their balance sheets are similar to the peer country average. However, the large New Zealand banks operate lower cost structures than both the small New Zealand banks and large banks in peer countries (table 2.2). The superior cost efficiency of large New Zealand banks relative to the smaller domestic banks is likely to be driven by greater economies of scale within large banks’ operations. Furthermore, New Zealand is the only country in the comparison group where all of the large banks are owned by larger overseas parents. This ownership structure is likely to provide further efficiencies and support to the large New Zealand banks, from which much of the rest of the comparison group does not benefit.12

- The Australian shareholders of the large New Zealand banks may require higher risk-adjusted returns on equity than shareholders of other banks. This is possible due to differences in the tax treatment of returns to shareholders in New Zealand and Australia. In particular, imputation credits received by Australian shareholders on dividends from New Zealand banks are not transferrable to the Australian tax system.13 In this instance, large banks would be expected to be more profitable than those in the rest of the sector, even in a competitive market.

- The differences in profitability may also be explained by other differences between the operational structure of banks in the comparison group and the regulatory environments in each country. For example, New Zealand banks engage in relatively little investment banking and funds management compared to some banks in peer countries. Investment banking generates significant revenue for these banks, but also contributes to higher cost ratios.

The benefits of profitable banks are particularly evident in the current environment, with New Zealand banks in strong positions to manage increasing stress in their lending books and a deterioration in global economic conditions. Importantly, profitability allows banks to support their customers by taking a long-term view in times of stress. It also enables the necessary investment in systems to improve efficiency and operational resilience. Therefore, profitability puts banks in a position to earn their social licence by contributing to a sound, efficient, inclusive, and dynamic financial system.

Table 2.2

Profitability of banks in New Zealand and selected large banks in peer countries1

(Figures are 5-year averages over 2018-2022)

| Country (number of banks) | Return on equity Net profit / CET 1 % |

= (Total income Net interest + other income / Exposure % |

- Total expenses) Expenses + tax / Exposure % |

x Leverage multiplier Exposure / CET 1 times |

|---|---|---|---|---|

| New Zealand large (4) | 15.28 | 2.09 | 1.21 | 17.4 |

| New Zealand small (5) | 7.35 | 2.07 | 1.66 | 17.6 |

| Canada (4) | 19.59 | 2.72 | 1.91 | 24.4 |

| Norway (3) | 13.91 | 2.05 | 1.12 | 15.1 |

| Singapore (3) | 13.66 | 2.11 | 1.20 | 15.0 |

| Australia large (4) | 12.87 | 1.94 | 1.33 | 21.0 |

| Sweden (4) | 12.75 | 1.68 | 1.08 | 21.4 |

| Australia small (3) | 10.28 | 2.00 | 1.49 | 20.3 |

| Switzerland (4) | 8.30 | 2.88 | 2.53 | 23.4 |

| Netherlands (4) | 8.28 | 1.75 | 1.36 | 21.4 |

| Denmark (4) | 7.03 | 1.21 | 0.91 | 22.7 |

| Ireland (4) | 4.82 | 2.33 | 1.99 | 14.1 |

| Peer country average (37) | 11.25 | 2.08 | 1.49 | 19.8 |

Source: Banks’ financial statements, RBNZ calculations. Country averages are exposure-weighted, while peer averages (last row in table) are the unweighted mean of countries.

Footnotes

11 The net interest margin (NIM) is the difference between a bank’s interest income and interest expenses, divided by its interest-earning assets (for example, loans to customers) to account for size. Net interest income is the primary component of New Zealand banks’ earnings, consequently, the NIM is a useful measure of how effective a bank is at generating income.

12 Understanding financial system efficiency in New Zealand (Bloor & Hunt, 2011)

13 Australian shareholders receive imputation credits with dividends from Australian banks, which reduces their tax burden and increases their after-tax return. However, the imputation credits received on dividends from New Zealand banks are not transferrable to the Australian system. Hence, Australian shareholders in banks with New Zealand operations require a higher return on equity from the New Zealand operations to receive the same after-tax return as the return on Australian operations.