We hold foreign reserves to respond to unlikely but extreme events. As the timing of these events is unpredictable, we must be ready and able to respond at any time.

To support the underlying purpose and objectives for holding foreign reserves, the primary principles for managing the portfolio of assets are safety (a low risk of issuer default) and liquidity (a low risk of not being able to sell the asset when needed).

Subject to these criteria being met, we will look to maximise returns. In practice, this means that the foreign reserves are mainly invested in government bonds from major advanced economies.

Balancing risks and costs of unhedged and hedged reserves

Our foreign reserves consist of 2 distinct portfolios:

- unhedged reserves

Find out more about unhedged reserves

- hedged reserves

Find out more about hedged reserves

The unhedged reserves are typically more costly to hold in normal times, where no intervention is occurring. This can expose our balance sheet to greater volatility due to fluctuations in the exchange rate. However, there are fewer risks associated when unhedged foreign reserves are used in an intervention event and the foreign reserves are sold.

Due to the market dynamics in the New Zealand dollar (NZD) cross currency basis swap market, hedged reserves are typically cheaper to hold in normal times, when no intervention is occurring and are not exposed to exchange rate fluctuations. However, there are potentially large refinancing risks associated with using the hedged reserves to intervene. This risk is why some central banks choose not to hold hedged reserves on their balance sheet.

Our aim is to balance these different costs and risks by holding a portfolio made up of both unhedged and hedged reserves. This decreases the cost of holding foreign reserves in normal times, without compromising our policy objectives. The composition of the foreign reserves is expected to vary over time in line with market conditions.

Read the related publications

Our approach to holding and managing our foreign reserves

Foreign reserves — why we hold them influences how we fund them

Managing open foreign exchange (FX) position

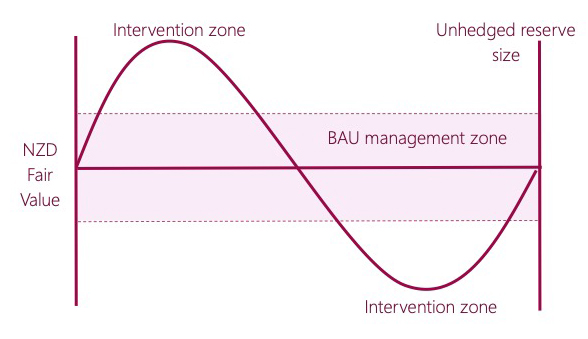

During normal times, we aim to manage the unhedged reserves portfolio or ‘open FX position’ around the exchange rate cycle. The management of the open FX position would normally involve us buying and selling small amounts of NZD when the traded value of the exchange rate deviates from our estimates of fair value. This means we would be selling NZD when the exchange rate is above our estimates of fair value and buying NZD when the exchange rate is below fair value. The actual amount of transactions conducted will also be influenced by other considerations such as risk tolerance and market conditions at the time.

Download the diagram showing how we manage our open foreign exchange position (94 KB)

{kind=link}

These transactions are not considered intervention as they are not intended to influence the level of the exchange rate, nor are they primarily driven by monetary policy or financial stability considerations. These transactions ensure that we effectively manage the open FX position over the long term and helps minimise the cost of holding unhedged foreign reserves.

Being active in the market also allows our staff to gather important market intelligence and maintain the skills required to intervene in the market if and when it is necessary.

The intervention zone

When the exchange rate is exceptionally high or low relative to economic fundamentals or estimates of fair value, the exchange rate may be in the ‘intervention zone’. This does not necessarily mean we would intervene as there are a number of criteria that we would need to meet.

Find out more about when we may intervene

Strategic Asset Allocation (SAA)

We follow the principles of safety and liquidity when investing foreign currency into foreign assets. Because of this, investments are restricted to highly traded currencies of advanced economies.

Hedged reserves

The current SAA benchmark for the unhedged foreign reserves includes 5 major currencies. To ensure that unhedged reserves are effective in meeting their purpose, we impose a number of restrictions on the portfolio before it is optimised to enhance risk adjusted returns. The restrictions may include maximum or minimum requirements for certain currencies to ensure that the portfolio maintains a very high standard of safety and liquidity.

Read the related publication

The currency denomination of New Zealand’s unhedged foreign reserves

Bank of International Settlements (BIS) investment funds

A small portion of the reserves portfolio is currently invested in investment funds managed by the BIS. These include the:

- Asian Bond Fund

- Chinese Yuan Bond Fund

- US Dollar Green Bond Fund.

These funds help diversify our foreign reserve portfolios while also supporting our other central banking objectives through our involvement in international central bank initiatives. These investments meet the liquidity and safety threshold required of the foreign reserves and do not compromise our objectives for holding foreign reserves.

Agreements with foreign official institutions

In addition to the holdings of foreign reserves, we have agreements with the People’s Bank of China (PBoC) and Hong Kong Monetary Authority (HKMA).

We have previously been offered temporary swap lines by the Federal Reserve Bank of New York, during periods of heightened volatility and USD illiquidity. This was most recently offered in April 2020 during the Covid-19 crisis, and expired on 31 December 2021.