Speech delivered to Citi Australia and New Zealand Investment Conference

On 16 October 2019, in Sydney

By Geoff Bascand, Deputy Governor and General Manager of Financial Stability

Good morning everyone,

My thanks to Citi for the invitation for me to come here today and speak with you all - it’s a pleasure to be here.

Today I'm going to start by setting the scene to give you an understanding of where the Reserve Bank of New Zealand is currently at in achieving both price and financial stability, and I'm also going to outline the risks that New Zealand is exposed to in a local and global environment.

Setting the scene

The Reserve Bank of New Zealand’s purpose is to promote the prosperity and wellbeing of New Zealanders, and contribute to a sustainable and productive economy. For this speech I want to mostly focus on how we promote sustainability by delivering on our objectives: price stability, maximum sustainable employment, and financial stability, and the tools we apply to help keep the economy productive.

Over the past thirty years, we have seen economic volatility decline following the introduction of inflation targeting, with prices becoming more stable and remaining at relatively lower levels (Figure 1).

Figure 1: The decline in inflation volatility during the inflation targeting era in New Zealand

Source: Stats NZ, RBNZ calculations.

Over this same period we have also seen improvements in economic growth, as well as less volatility in this growth (Figure 2).

Figure 2: Quarterly real GDP growth before and during the inflation targeting era

Source: Stats NZ, RBNZ calculations.

With monetary policy maintaining price stability and supporting maximum sustainable employment, other policies we have are aimed at maintaining financial stability. What we mean by ‘financial stability’ is having a financial system that can withstand severe, yet plausible, shocks and avoid financial crises. These crises can destabilise economic activity and severely impact business and household income. Indeed, evidence from a wide range of countries over many decades shows us that when crises do happen, they are immensely damaging and can have long-lasting effects.1

Usually our price stability and financial stability policies are complementary. However, the low interest rate world we live in complicates achieving both of our objectives, encouraging a build-up of leverage in the financial system. The persistent decline in long-term and short-term interest rates has supported very high levels of private sector leverage.

As shown in Figure 3 below, the credit to GDP ratio in New Zealand remains very close to that observed just prior to the Global Financial Crisis (GFC).

Figure 3: Declining interest rates and increasing debt levels

Source: Stats NZ, RBNZ calculations.

Household debt as a proportion of disposable income has risen from 60 percent in the early 1990s to 166 percent across all households, and for households with mortgages, the increase is even larger (Figure 4).

Figure 4: Debt to disposable income ratio in New Zealand

Source: Stats NZ, RBNZ Household Assets and Liabilities Survey, RBNZ estimates.

It’s important to remember that while extremely low interest rates have been commonplace in the developed world for over a decade now, New Zealand’s very low interest rate environment is a more recent phenomenon. The Official Cash Rate (OCR) only dipped below 2 percent (year average) in November 2016.

We know that some academic studies suggest that expansionary monetary conditions can encourage lower lending standards and higher levels of leverage in the financial system.2 And, as we transition into this very low interest rate environment, we will continue to monitor such vulnerabilities in New Zealand.

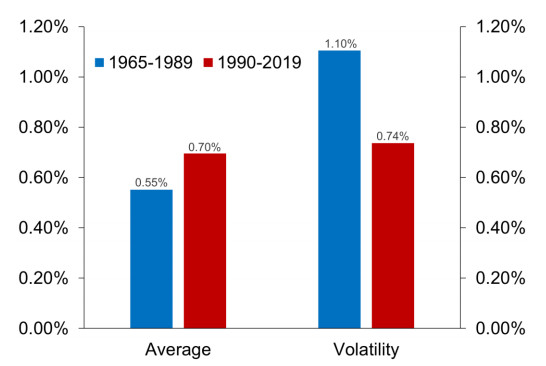

We recognise that the risks globally are high, and New Zealand is particularly vulnerable to external events. Our economy is quite small - less than a fifth of the size of the Australian economy, and just like Australia, New Zealand is heavily reliant on commodity exports and is very open to financial capital flows. Commodity price movements in world markets determine the value of our key exports, as well as the price we pay for our imports, particularly those that are fuel-related. Monetary policy moves by foreign central banks may generate unfavourable fluctuations in our exchange rates.

However, as Figure 5 demonstrates, the New Zealand economy has responded much more than Australia to downswings in the global economy. In contrast to Australia, economic activity in New Zealand contracted during the Asian crisis in the late 1990s, and the US subprime mortgage crisis of the late 2000s that snowballed into the GFC. This is despite the fact that the Australian terms of trade has been through dramatic escalations and downturns, while New Zealand’s terms of trade has experienced relatively less volatility around an upward trending path (Figure 6).

Figure 5: Economic activity in New Zealand and Australia in the inflation targeting era

Source: Haver Analytics, RBNZ calculations.

Note: The data has been normalised to 100 in 1990 Q1.

In addition to the disruptions in the global economic environment, the New Zealand economy is occasionally affected by weather-related shocks, such as droughts, that constrain the agricultural sector. In the past, we have also suffered severe damage to our infrastructure due to earthquakes.

So when the Bank sets monetary and financial stability policy, it needs to balance concerns about these different- and sometimes conflicting - domestic and international influences.

Figure 6: The terms of trade in New Zealand and Australia in the inflation targeting era

Source: Haver Analytics, RBNZ calculations.

Note: The data has been normalised to 100 in 1990 Q1.

Mortgage lending in New Zealand is dominated by floating and short one to two-year fixed rate mortgages (Figure 7). This implies that the changes in the domestic policy rate and international bank funding market rates pass through to the effective mortgage rates relatively quickly, and influence the demand for housing and house prices in New Zealand.

Figure 7: Time to re-price on housing loans in New Zealand

Source: RBNZ Bank Balance Sheet Survey, RBNZ Standard Statistical Return, RBNZ calculations.

When interest rates are low, households can accommodate a higher level of debt for given incomes; though they remain susceptible to adverse macroeconomic shocks.3 For example, if bank funding costs escalate due to distressed offshore funding markets, lending rates in New Zealand would rise, and households may find it hard to service debt.

On another front, elevated dairy prices encouraged investment in dairy farms, leading to high debt levels in the agricultural sector. It’s worth noting that agricultural debt in New Zealand has increased from $5 billion in 1990 to $63 billion today. Two thirds of this debt is owed by dairy farms. If New Zealand’s agricultural export revenue fell due to a weakening of global demand or a domestic drought, the contraction of economic activity in that sector could spill over to lower income and spending in the household sector, thereby increasing debt defaults.

That’s why maintaining financial stability in this highly vulnerable environment is challenging. Minor events appear manageable, but we need to be prepared for major shocks, and it is here that our financial stability policies are centred, including our proposals to increase bank capital requirements.

The Reserve Bank of New Zealand’s approach to financial stability

Our approach to financial stability is dynamic, and we focus on building financial system resilience (Figure 8). We recently renewed our approach to financial stability4 to recognise that the financial system is constantly evolving, as are the risks and challenges. Our baseline settings are not set-and-forget, we adapt them as risks and the resilience of the financial system evolve.

Figure 8: The Reserve Bank’s approach to financial stability

Based on our understanding of the financial system, we can enhance resilience by establishing rigorous baseline requirements and adapting them as necessary. Table 1 lists the range of prudential and macro-prudential instruments available to us. For example, we can increase capital buffers for banks, or we can tighten Loan-to-Value Ratios (LVRs) if risks related to household indebtedness are excessively heightened. We can also adjust liquidity requirements for banks to ensure they remain solvent.

As a central bank, it’s imperative that we have a full range of tools that we can use if needed to ensure the financial system remains stable.

Table 1: The Reserve Bank’s prudential toolkit

|

Crisis Prevention

Crisis Management |

Purpose | Relevant tools | Impact on financial system resilience | Impact on wider economy |

Supervision, oversight and disclosure |

|

Macroprudential policy Reduce risk that the financial system amplifies a severe economic downturn |

Borrower restrictions (LVRs) |

Reduced losses in a severe economic downturn | More resilient households and banks reduce severity of an economic downturn | ||

| Capital and liquidity instruments (CCyB/SCR) | Lowers incentives on banks to deleverage in a downturn; supports higher credit supply and economic activity | ||||

|

Prudential Policy Maintain baseline resilience of the financial system |

Capital buffers | Banks remain solvent through the economic cycle | Maintains market confidence and lowers risk of sudden increases in funding costs for households, businesses and the economy. | ||

| Liquidity policy | |||||

| Governance and local incorporation | |||||

| Manage and limit impact of distress or failure | Collateral standards |

Banks remain functioning parts of financial system

Losses absorbed first by shareholders |

Maintains availability of credit and banking services necessary for economic activity

Mitigates costs for creditors and tax payers |

||

| Outsourcing | |||||

|

Open Bank Resolution

Minimum capital |

Depending on the situation, we choose the appropriate regulatory tool to address the identified risk to financial stability, bearing in mind efficiency costs, the level of effective self and market discipline, and the regulatory framework as a whole. We adapt tools in response to unsustainable booms in credit and asset prices in order to reduce the likelihood of crises.

But crisis prevention is by no means assured. As history tells us, crises come from unexpected sources and are hard to predict. So we need robust standards to maintain resilience. Minimum capital and liquidity requirements are essential tools for this purpose. We also need tools to manage the consequences if our financial institutions are unable to survive a period of stress or crisis – our crisis management regime that is under review as part of Phase 2 of the Review of the Reserve Bank Act.

Our holistic approach to macroeconomic and financial stability

As I mentioned earlier, the New Zealand economy is in a good space. Since the beginning of inflation targeting, macroeconomic volatility in general has declined. Inflation is just below the mid-point of the target band, and employment remains around its maximum sustainable level. But we are wary of potential challenges to macroeconomic management.

The OCR is currently set at 100 basis points, a historically low level in New Zealand, in order to achieve our monetary policy objectives. Lower rates still may be needed to achieve our inflation and maximum sustainable employment objectives. The Reserve Bank is undertaking further preparatory work on less conventional monetary policy tools5 that are available, in the event that the policy rate is pushed down to its effective lower bound. Novel monetary policy tools, such as large scale asset purchases and targeted term lending that have been previously used in the United States and the United Kingdom, are tailored to support economic activity by strengthening credit growth.

However, a highly stimulatory monetary policy stance may lead to over-exuberant levels of credit growth, and as seen in empirical studies in the international literature, may lead to lower lending standards. If looser monitoring standards prevail on the supply of credit, the macroeconomic costs of a severe downturn may be amplified. Macroprudential policy can help to manage the movements in credit so as to ensure that macroeconomic booms and busts are not excessively volatile.

Our assessment of financial stability risks is more nuanced than debt levels per se. We look at the distribution of debt as well as its growth rate, and the sustainability of the asset values it is attached to. While we are concerned about the levels of debt in parts of the household and agriculture sectors, there is scope for more borrowing and investment to take place in less leveraged areas. Our restrictions on high loan-to-value ratio (LVR) lending (one measure of high risk lending) are one tool we have that can moderate financial stability risks even while the stock of household debt is rising.

More capital is a key part of building New Zealand’s economic resilience

In December 2018, we proposed to increase bank capital requirements in New Zealand, to increase the overall resilience of the banking sector to economic shocks. We proposed that the capital framework should be set so that banks have sufficient capital to withstand a 1-in-200 year event.

Some have questioned why we are proposing this increase in capital, given the perceived impacts it could have. So let me explain - first and foremost, from a societal point of view, setting capital requirements is a long-term game. The benefits of more capital essentially result from avoiding future economic and social costs that would arise from a financial crisis and resulting economic recession (Figure 9).

Figure 9: A conceptual framework relating financial stability to economic output

We targeted a high level of resilience to withstand severe shocks because the costs of severe crises are very high, while international evidence indicates that the costs of buying additional insurance are modest. Moreover, we would transition to this higher level of resilience over time.

For shareholders, the increased equity funding may result in lower returns per dollar invested, but the flip side for them is a safer investment. Also, it is worth recalling that capital requirements aren’t like other regulations, in that they don’t create an ‘expense’ for banks. Indeed, in an accounting sense, interest expenses would reduce for the same level of funding. And as with most investments, less leveraged businesses earn lower but more stable returns. We anticipate the same for banks to an extent, and past history does indeed suggest there is a relationship (Figure 10).

Figure 10: Return on Tier 1 Capital, and Tier 1 Capital to tangible assets (locally incorporated banks)

Source: RBNZ GDS Survey Data, RBNZ calculations.

Determining appropriate capital requirements is, of course, more than just counting the benefits. The upsides must be balanced against the downside of higher interest rates. We’ve anticipated that there will be a 20 to 40 basis point increase in bank margins in the long term as a result of these proposals.6 While these are relatively small numbers, they will ultimately have an impact on investment and spending in the New Zealand economy.

Our approach from the outset has been to set capital requirements at a level where we can be confident that these costs are outweighed by the benefits of a safer financial system.

To calibrate our proposals for New Zealand, we drew on many pieces of analysis. These included international literature, stress test results and historical New Zealand data on bank losses and loan performance.

Currently we are reviewing all inputs and modelling assumptions, and carefully assessing submissions, before finalising the plans that will be announced in December. As well as the overall level of capital, we are also re-examining all other aspects of the Review, such as the quality of capital (capital instruments) and the transition path to the new requirements.

A well-capitalised banking system also means that our banks will be able to access global funding markets, even in stressed conditions

While higher levels of bank capital cannot stop economic fluctuations, it can help banks with even the more moderate downturns, not just the 1-in-200 year event we calibrate to. Research suggests that well-capitalised banks have easier access to funding than their more leveraged peers during turbulent times. 7 For the economy, this means a weakly capitalised banking system can undermine monetary policy responses to economic downturns as banks may struggle to pass through lower interest rates with their cheaper funding sources drying up.

Conversely, a well-capitalised banking system is less likely to face funding issues during these downturns and we would anticipate a much more orthodox response to monetary policy in the economy. Bank capital requirements also can have a more direct role in responding to these economic fluctuations through a counter-cyclical buffer.

Having a well-capitalised banking system in New Zealand, given we are a net importer of capital, also means that our banks – and the wider economy - will be able to continue to access global funding markets even in times of financial stress.

Of course, we are listening to what others are saying about our proposals. We’ve been consulting with the public and many of our stakeholders to fully understand the impacts they believe an increase to capital requirements will have. We’ve commissioned three internationally recognised experts to review the proposals, which have been published on our website. All of these views have been captured and are being considered, and if we’ve got it wrong, we’ll make adjustments to reflect that because it’s important that we get this right.

The international dimension

We set our capital requirements according to the New Zealand specific risk environment, but we also acknowledge how we ‘stack up’ internationally, and why we may need a more capitalised banking system than those in other countries.

We have previously compared our proposed capital levels with Basel Committee estimates and Standard and Poor’s (S&P) methodology, placing our proposals around the top quartile. 8 Since September 2019, S&P’s assessment of economic risks in New Zealand has improved. They viewed that the moderation of house prices since 2017 has reduced the likelihood of a severe house price correction and with it, the potential losses banks may face in such a scenario – that’s good news. Our financial stability risks have reduced due to a slowing housing market, and our LVR policy has contributed to that.

The improved country rating means that the New Zealand banks’ capital positions using S&P’s risk-adjusted capital (RAC) ratio have improved.9 Our Capital Review proposals would mean that the banks’ S&P RAC ratios would increase further still, towards being among the best capitalised banks across a range of peer countries (Figure 11).

Figure 11: S&P RAC ratio – comparison of the four largest New Zealand banks to large banks in peer countries (October 2019)

Source: Standard and Poor’s, RBNZ calculations.

Notes: New Zealand (post-CR) shows an estimate of the RAC ratios of the four largest New Zealand banks assuming the Capital Review proposals are implemented as consulted on, plus a 1% management buffer. Comparator banks include Erste Group, Raiffeisen Bank International, Bank Austria (Austria), ANZ Banking Group, Commonwealth Bank, National Australia Bank, Westpac Banking Corporation (Australia), Česká spořitelna, ČSOB, Komerční (Czechia), Danske Bank, Jyske Bank, Nykredit Realkredit (Denmark), Nordea, OP Corporate (Finland), Bank of East Asia, Bank of China (HK), Hang Seng Bank, Hongkong and Shanghai Banking Corporation, ICBC (Asia), Standard Chartered HK (Hong Kong), Allied Irish Banks, Bank of Ireland, Permanent TSB (Ireland), Hapoalim, Leumi (Israel), Arion, Íslandsbanki, Landsbankinn (Iceland), ABN AMRO, ING, Rabobank (Netherlands), DNB Bank (Norway), ANZ New Zealand, ASB Bank, BNZ, Westpac New Zealand (New Zealand), SEB, Handelsbanken, Swedbank (Sweden), DBS, OCBC, UOB (Singapore).

We realise that the slowdown in the New Zealand housing market may be a cyclical rather than a structural change. In the longer term, we remain vulnerable, especially if household indebtedness continues to grow. This is why we need policies that aim to ensure enduring resilience in the financial system. Indeed, in their assessment, S&P note that New Zealand’s economic imbalances remain somewhat elevated because of persistent current account deficits, high external debt, and an economy that is exposed to fluctuations in commodity prices.

Relationship with Australia

Our conservatism, relative to Australia, in our bank capital proposals reflects the higher macroeconomic volatility that we have endured, as I pointed out earlier. However, we have been, and will continue to work closely with APRA. We continuously update one another on our prudential regulations, we maintain a strong working relationship, and we also respect each other’s objectives as regulators aiming to protect our respective financial systems.

Conclusion

With New Zealand’s macroeconomic policy framework and strong financial sector soundness, investors can have long-term confidence in New Zealand as an investor destination. The prospects of sustainable and productive growth are enhanced through predictable macroeconomic policy settings and avoidance of financial crises.

Economic and other shocks have constrained New Zealand’s economic performance historically. Although our macroeconomic stability has improved in recent decades, we remain vulnerable to external and domestic disturbances. Overall debt levels remain high while the concentration and persistence of high-leverage within segments of the household and agricultural sectors questions the quality of banks’ lending standards.

The more enduring that low interest rates are, and the more successful they are in promoting borrowing and investment, the more they are likely to pose challenges to the Reserve Bank’s financial stability objectives.

The Reserve Bank has a number of tools it applies to manage financial stability risks, and its LVR policies have a role in limiting the risks that could arise from increasing leverage through inadequate lending standards.

More capital is a key part of building New Zealand’s economic resilience for when severe shocks do occur. We are in the process of weighing up the costs and benefits of how much more and the type of capital that is appropriate for the desired level of resilience, and the timeframe to achieve it. Decisions on the Capital Review are expected to be released in the first week of December.

Footnotes

1 See the discussion of economic and social costs in Bascand (2018)

2 Some of the literature exploring this connection includes Neuenkirch and Nöckelb (2018), Dell’Ariccia, Laeven and Suarez (2017), Jimenez, Ongena, Peydro and Saurina (2014), and Caballero, Hoshi and Kashyap (2008).

3 See also the Australian case in Ellis and Littrell (2017).

4 See Bascand (2019)

6 Two of the External Experts, Dr James Cummings and Professor David Miles, suggest that these estimates may be on the higher side of what is plausible due to the cost of equity being overstated. The summary, as well as their reports, are available on the Capital Review webpage. Capital reviews

8 Bascand (2019b)

9 S&P calculates its own risk-adjusted Tier 1 capital ratios for many banks around the world, using a methodology that attempts to reduce the influence of differing national applications of the Basel framework while still taking into account the different risk profiles of the countries in which each bank operates.