Good morning and thank you for the opportunity to meet with you again, it’s a great pleasure to be here. I believe this is the 23rd year in which the Reserve Bank has been invited to meet with the Canterbury Employers’ Chamber of Commerce and offer some thoughts on the state of the economy.

If it is helpful I’ll start with a few comments on the global economy, before turning to the domestic economy, the Policy Targets Agreement and the outlook for monetary policy.

The global economy

Last year the global economy hit a soft patch and financial markets have had a rocky start to the current year. Global growth, at 3.1 percent, was the slowest since 2009 despite unprecedented monetary stimulus and falling oil prices. This wasn’t the first slowdown since the Global Financial Crisis (GFC), although previous episodes have largely occurred in the advanced economies, such as in the EU area in 2012. Indeed, the emerging and developing countries, led by China, have delivered a strong growth performance in recent years, accounting for about 80 percent of global growth since 2010 (measured in purchasing power parity terms)[1].

This pattern began to change in mid-2014 with weaker trade volumes and slower growth in emerging markets – and especially in China, Russia, Brazil and South Africa. During 2015, foreign net capital outflows from emerging markets totalled USD 735 billion, the majority of which was out of China – the largest amount since 2008[2]. Growth picked up in the advanced economies – particularly in the US and European Union.

The slowdown in global growth hasn’t been for lack of monetary stimulus by central banks. In the history of the world as we know it, monetary conditions in recent years have never been easier.[3]

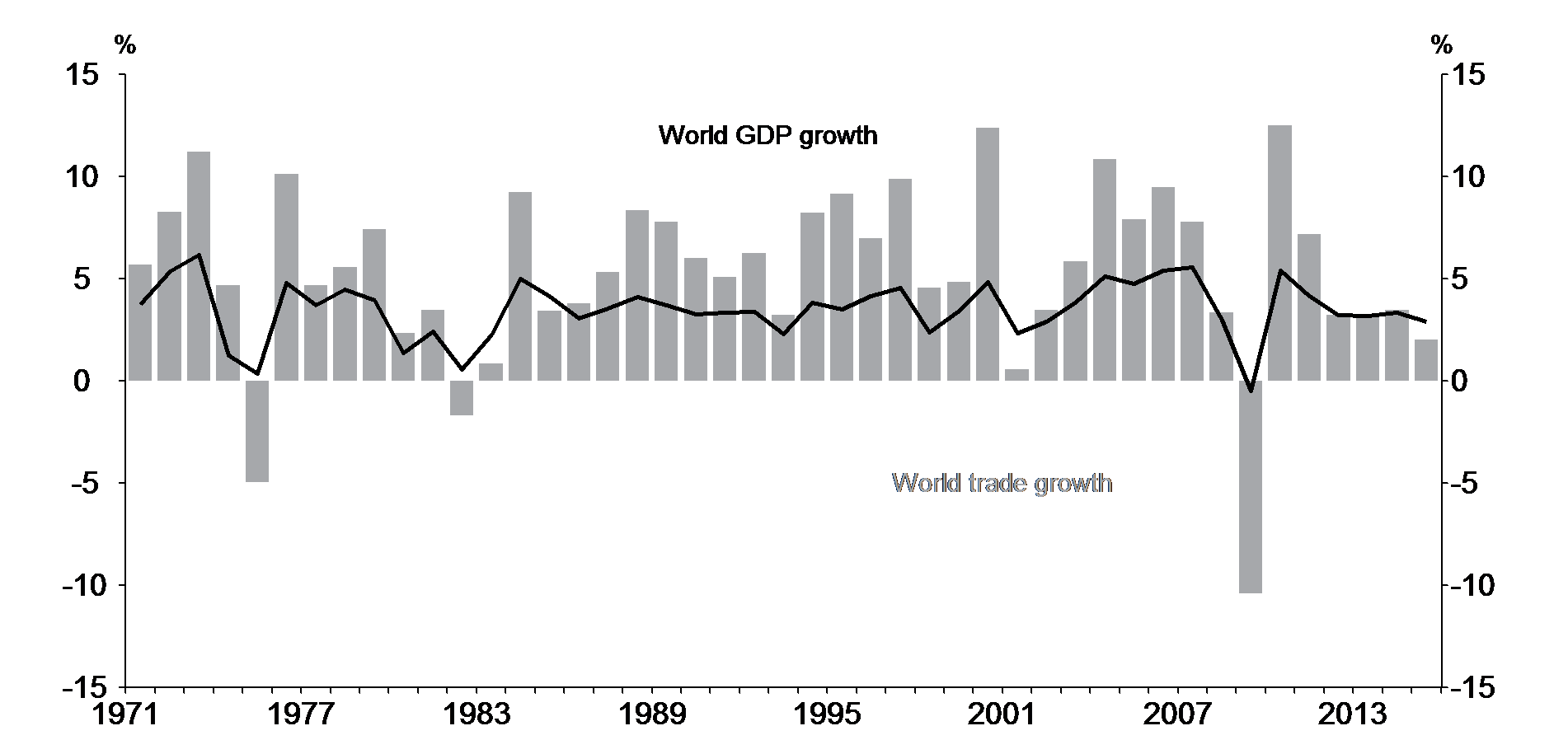

A particular concern during 2015 was the slow growth (2 percent) in the volume of merchandise trade. Since the mid-1960s there have only been five occasions of weaker trade growth – each was associated with a major slowdown in global GDP growth (OPEC1, OPEC2, Asia Crisis and US high tech bubble, and the GFC)[4]. The current weakness in trade volumes reflects the sluggish recovery in investment in advanced economies, slower growth in emerging markets, high inventories of commodities, and reduced import intensity in China. The Baltic Dry Index, which measures the cost of shipping raw materials such as minerals and grains, has fallen nearly 70 percent since the end of July 2015 and is at its lowest level since the index was established 30 years ago.

Figure 1: World trade volumes and GDP growth

Source OECD

Forecasts of global GDP growth in 2016 look a bit more promising with the IMF, World Bank, BIS, and OECD forecasting growth of between 2.9 and 3.4 percent. However, if world trade remains depressed and market volatility continues, we are likely to see downward revisions to these forecasts.

These institutional projections show improving growth in most advanced and emerging market countries (although with slower growth in China) and a pickup in world trade. All institutions see the balance of risks lying on the downside, with the main risks being:

- Monetary policy in the three largest central banks is on a divergent path with the Federal Reserve having begun to raise the Fed Funds rate, while further monetary easing is possible in the euro-area and Japan. This policy divergence could lead to greater financial market volatility and uncertainty.

- The weakness in commodity prices could be greater than projected and further reduce growth in commodity producers such as Brazil, Chile, Mexico, Russia, Saudi-Arabia and South Africa.

- A further slowdown in China could feed through into lower demand and production in China’s many trading partners. For example, 10 percent of the European Union’s exports and 18 percent of Japan’s exports go to China.

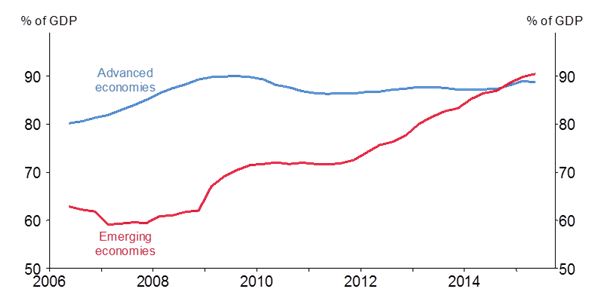

- The rapid build-up in non-financial corporate debt and falling corporate profitability in emerging markets pose risks to banking systems and to broader stability in these economies. Non-financial corporate debt in emerging market countries has increased from 60 percent of GDP to 90 percent of GDP since early 2009. At the same time, average emerging market profitability fell sharply in 2015 and is at its lowest level in a decade.[5]

Figure 2: Non-Financial Corporate Debt

Note: The advanced economies group contains Australia, Canada, the euro area, Japan, Sweden, Switzerland, the United Kingdom and the United States. The emerging economies group contains Argentina, Brazil, China, India, Indonesia, Korea, Mexico, Poland, Russia, Saudi Arabia, South Africa and Turkey.

Sources: IMF, Bank for International Settlements.

At the country level, China represents the greatest risk to global growth given its impact on global trade volumes and commodity prices, the rapid build-up in corporate indebtedness and the difficult switching strategy (away from investment and manufacturing towards stronger private consumption and services) that is underway. China accounted for 40 percent of global growth in 2014. Although its output is 60 percent of that of the US (at market exchange rates), imports of non-oil commodities are around 2½ times those of the US. Market forecasts suggest that China’s economic growth is currently in the 5 to 7 percent range and supported by strong services sector production, whereas growth in activity in the manufacturing and construction sectors has slowed substantially.

An area to watch closely is the rapid rise in China’s corporate indebtedness. At around 220 percent of GDP, China’s debt burden is not the highest among the largest economies, but the extent of its debt accumulation (over 70 percent of GDP in 6 years) is unprecedented. Most of the increase represents SOE debt, mainly in the areas of real estate, construction, mining and utilities. Many of China’s 155,000 SOEs are losing money, leverage has soared, and the average return on assets is low and falling. A key challenge will be how to begin the necessary deleveraging process without causing a major slowdown in growth.

Simulations by the OECD suggest that a reduction of 2 percentage points in Chinese domestic demand growth over the next two years, if accompanied by the types of financial market impacts on equity prices and uncertainly and risk premia that we observed in August last year and again more recently, would lower global growth by ¾ - 1 percentage point on average in 2016-2017[6]. Its impact would be greater if this were accompanied by a sizeable and prolonged depreciation in the RMB that exports deflation to the rest of the world.

Outlook for the New Zealand Economy

Our economy has faced a wide range of shocks since the GFC, some positive for growth, some negative. A partial list includes: the tightening in global liquidity in the immediate aftermath of the GFC; the Canterbury earthquakes; 2012/13 drought; terms of trade that reached a 40 year high; the 70 percent peak to trough movement in dairy prices; the 75 percent fall in oil prices; record net migration and labour force participation; sizeable movements in the real exchange rate and annual house price inflation in Auckland that reached 27 percent. Overall, the economy appears to have done reasonably well despite the headwinds created by some of these developments.

The economy is in its 7th year of expansion. Annual GDP growth slowed to around 2½ percent in the first half of 2015, primarily due to the sharp decline in dairy prices, but the economy is projected to grow at around 3 percent over the next couple of years. At this stage there is nothing to suggest that the expansion will stop. However, more so than in recent years, there are greater uncertainties around the outlook, and, as with the global economy, the balance of risks lies on the downside. Foremost among these are the possibility of slower growth in China, weaker than projected dairy prices, and the implications of a serious El Niño event (although it appears that this threat has eased due to higher rainfall in recent weeks). The main upside risk is around the possibility of continuing strong migration inflows.

Slower growth in China

A marked slowdown in the Chinese economy would have important implications for New Zealand, especially if accompanied by a sharp decline in China’s household consumption. This would reduce the volume and price of our commodity exports to China, and likely affect our services trade, including exports of education services and tourism. Its overall impact on our economy would be magnified through other trade channels as China is the largest trading partner for over 100 countries – including our main trading partners.

El Niño

New Zealand is experiencing El Niño weather conditions. Its impact on the economy will depend on whether it leads to drought conditions and, if so, where the drought hits and how long it lasts. A prolonged drought would lower agricultural production and reduce farm incomes. New Zealand’s last major El Niño occurred in 1997, and like the 2013 drought, reduced GDP by around ¾ percent.

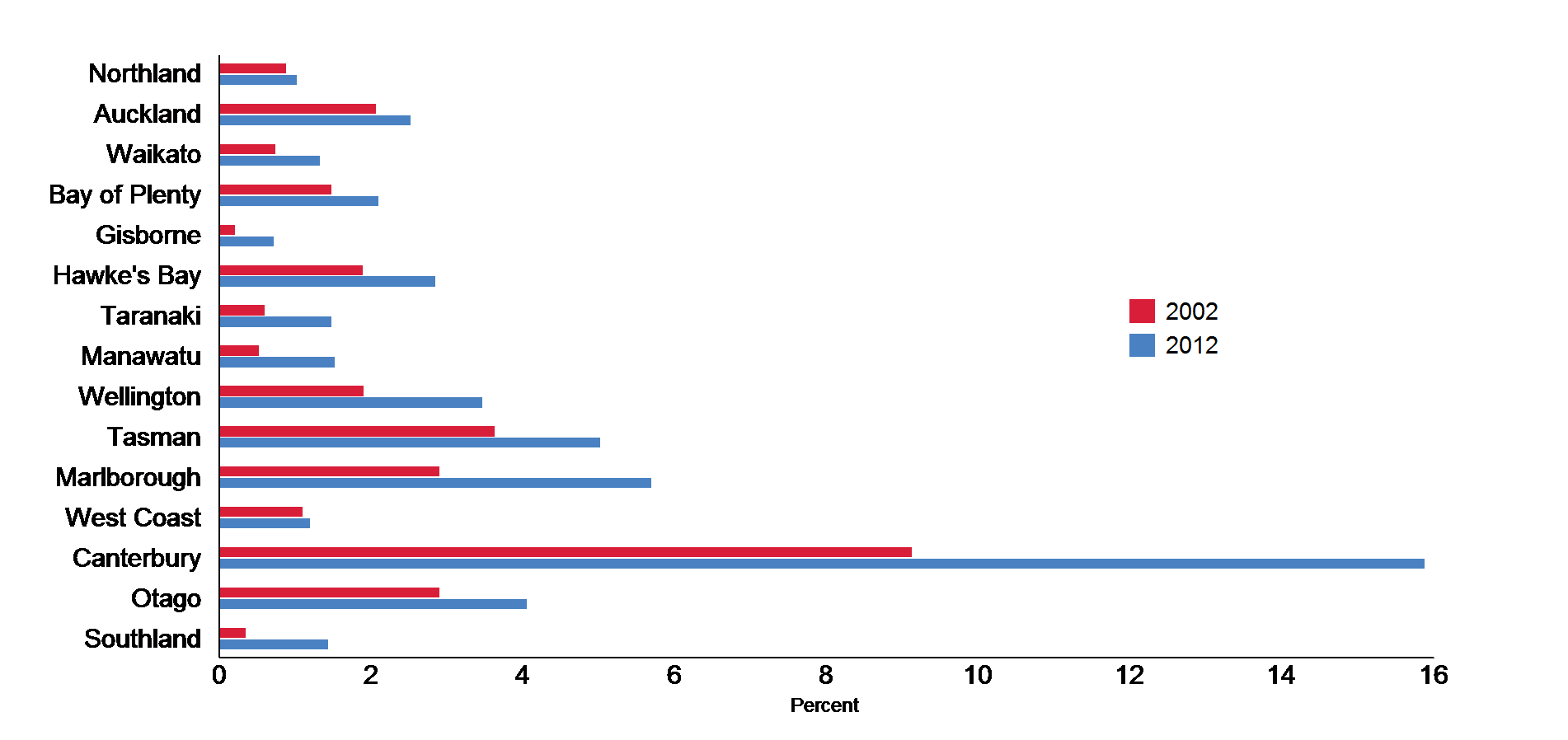

Farming patterns however, have changed considerably since the 1997 El Niño event. Since 1996, the dairy herd has increased by 61 percent, while sheep and beef numbers have fallen by 37 percent and 24 percent respectively. Dairy numbers have expanded in Canterbury, Southland, Waikato and Otago with much of the growth in Canterbury facilitated by extensive investment in irrigation. The severity of the 2012/13 drought reflected its impact in Northland, Waikato and the Manawatu – areas with heavy concentrations of dairying, but limited irrigation.[7]

Figure 3: Irrigation by region (share of total hectares farmed)

Source: Statistics New Zealand Agricultural Census

Dairy Prices

Most dairy farmers have experienced two consecutive years of negative cash flows and cut back their spending. Our December 2015 MPS projections assumed that the price of wholesale milk power would rise gradually and reach USD 3300/metric tonne by mid-2018. The current auction price of USD 2188/metric tonne remains well below this level. Farm gate prices are falling in the US and Europe causing milk production to slow, while Fonterra expects production in New Zealand to decline by around 6 percent in the current season. Last week, Fonterra reduced its pay-out estimate for this season by 10 percent.

Net Migration

Over the past 3 years net permanent long-term migration has totaled 133,000. The December MPS projections assumed that we are about half way through the current migration cycle, which would make it the strongest net migration surge for several decades. However, there is considerable uncertainty around the magnitude of future flows given the difficulty in forecasting arrivals. A stronger or more persistent net migration inflow would create demand pressures, but also raise the economy’s supply potential. The impact on consumer price inflation would depend on how quickly the supply response (eg from the growth in labour force) offsets the additional demand generated by the net migration. However, property prices in the Auckland market and elsewhere would be pushed further upwards.

Policy Targets Agreement

While the Policy Targets Agreement (PTA) for monetary policy is a relatively simple document, we continue to be surprised at the wide range of interpretations that we see in the media and in commentaries. I would like to take this opportunity to discuss: what the PTA says; the thinking behind the changes introduced in 2012; and how the Reserve Bank interprets the PTA –particularly in relation to recent data on inflation outcomes, and in relation to monetary policy going forward.

What the 2012 PTA says

The PTA has several important features, including:

- A well-defined policy target to keep future CPI inflation outcomes between 1 percent and 3 percent on average over the medium term, with a focus on keeping future average inflation near the 2 percent target mid-point.

- Recognition that inflation might deviate from its trend for several reasons such as international commodity price movements, natural disasters and government tax and other policy measures that affect prices.

- A requirement that the Bank monitor asset prices, have regard to the efficiency and soundness of the financial system and seek to avoid unnecessary instability in output, interest rates and the exchange rate.

Considerations underpinning the 2012 PTA

The 2012 PTA, which was signed by the Minister of Finance and myself in September 2012, recognises the flexible approach needed in making monetary policy decisions. Several considerations were important in this regard.

- The 1 to 3 percent target range remains the central focus of the Bank’s flexible inflation targeting framework, as has been the case since 2002. The range was deliberately framed in a medium term context, with an ‘on average’ connotation and recognized that inflation might move outside this band due to global developments in commodity markets, natural disasters, and/or government fiscal and regulatory decisions.

- The concept of a mid-point objective was introduced with the objective of helping to lower and stabilise inflation expectations close to 2 percent. This was important because CPI inflation had averaged 2.3 percent since 2000 and measures of inflation expectations were averaging 2.5 percent or higher. The language deliberately emphasised the medium-term context of the mid-point objective. This was because attempting to move rapidly to a mid-point target could create damaging volatility in output and key relative prices, including asset prices, that could, in turn, threaten financial stability and undermine longer-term growth prospects.

- The requirement that the Bank monitor asset prices was inserted for two related reasons. First, because of concerns at the rapid house price inflation and spillover into spending that New Zealand experienced in the mid-2000s (which was a key consideration behind the steady increase in the OCR during the mid-2000s that peaked at 8.25 percent in July 2007). Second, was the desire to avoid the serious economic and social damage caused by sharp falls in house prices that many economies experienced during the GFC.

- In a similar vein, the addition of the phrase requiring the Bank to ‘have regard to the efficiency and soundness of the financial system’, recognised that interest rates affect the demand for credit, and therefore the balance sheets of households and financial intermediaries. The language requires the Bank to consider whether its monetary policy choices could undermine the efficiency and stability of the domestic financial system.

Recent Inflation data

- Annual headline CPI inflation is currently 0.1 percent. Headline inflation is falling nearly everywhere across the globe, and is below the target range in nearly all of the 30 or so economies whose central banks pursue flexible inflation targeting.

- Headline inflation in New Zealand is below the 1 to 3 percent band primarily because of negative tradables inflation caused by the slow global economic recovery and the 75 percent decline in oil prices that has taken them to a 13 year low. Domestic petrol prices at the end of 2015 were 8 percent lower than a year ago, reducing CPI inflation by 0.4 percentage points. In addition, the Government’s decision to reduce motor vehicle levies has taken 0.3 percentage points off the CPI.

- Annual core inflation, at 1.6 percent, is consistent with the target range.[8] This is a useful measure of underlying inflation because it excludes one-off or highly volatile price movements that do not reflect fundamental sources of underlying inflation pressures.

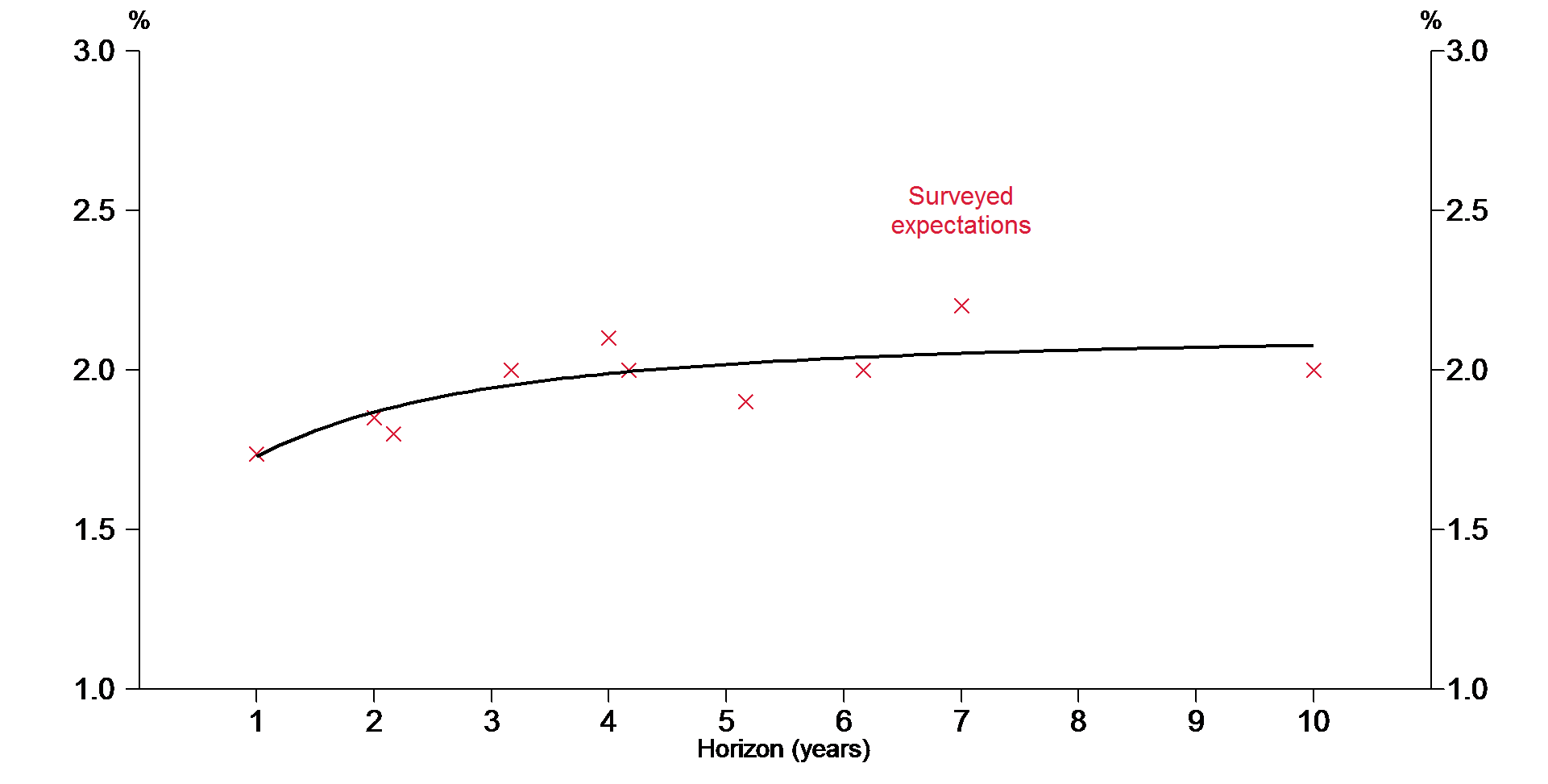

- Survey measures of inflation expectations have fallen and are now consistent with inflation settling at 2 percent in the medium term.

Figure 4: Inflation expectations surveys and fitted curve

Source: ANZ Bank, Aon Consulting, Consensus Economics, RBNZ estimates

- Non-tradables inflation is running at an annual rate of around 1.8 percent, but has been a little lower than forecast in recent years. This has also been the case in other advanced economies. Part of the reason is because the Phillip’s curve, which shows the relationship between unemployment gaps and annual CPI inflation, has flattened since the 1990s.

Figure 5: Annual CPI inflation and unemployment gap

Source: Statistics New Zealand, RBNZ estimates

The flatness of the relationship, in contrast with the clear negative relationship during the 1970s and 1980s, means that the economic recovery has translated into less inflation than historically might have been the case.

There are several possible explanations for the flatness of the relationship. These include: inflation expectations embodied in wage and price setting behavior have fallen and become more stable; globalisation and increased competition from offshore is limiting the ability of businesses to raise prices; and greater labour mobility, high levels of net immigration, and concerns about job security may mean that workers do not press as much for higher wages when domestic demand increases. Over the past three years, higher than expected immigration appears to have been an important factor in moderating labour market pressures and wage outcomes.

Monetary Policy Going forward

In balancing risks and making judgements about monetary policy we view the PTA flexibly, rather than taking a mechanistic approach. This is necessary in view of the numerous factors the Bank is required to consider - such as asset prices, financial stability and efficiency, volatility in output, interest rates and the exchange rate. All of these factors have bands of uncertainty attached to them. There are also considerable uncertainties associated with economic forecasting, and uncertainties as to which transmission channels monetary policy will operate through and the lags involved in achieving desired outcomes.

The Bank’s main influence over inflation comes through its scope to influence the economy’s output gap and the degree of non-tradable inflation (which accounts for around half of the regimen that makes up the consumers price index). Monetary policy can also at times have a significant effect on inflation through its influence on the exchange rate and tradables prices. There are major structural forces acting to reduce inflation that domestic monetary policy cannot influence. These forces, arising typically from trends in globalisation, information technology and demography, have exerted substantial downward pressure on global inflation in recent years.

Monetary policy also needs to work alongside other policies that can affect output growth and activity in markets, such as the housing market. For example, the Government’s fiscal policy has been contractionary in recent years and the regulatory framework around the housing market affects the supply and demand dynamics within that sector.

Annual headline inflation is currently 0.1 percent. This is primarily because of the negative inflation in the tradables sector, and the decline in oil prices in particular. Low oil prices are recognised in the PTA as a factor that can legitimately cause inflation to be outside the target band. It would be inappropriate to attempt to offset the low oil price effect through the OCR, which tends to influence inflation outcomes over an 18 month to 2 year horizon.

Our goal is to anchor inflation expectations close to the mid-point of the price stability target range, while retaining discretion to respond to inflation and output shocks in a flexible manner. In this regard, some recent inflation indicators are encouraging. Annual core CPI inflation, at 1.6 percent is well within the target range, and the Bank’s combined measures of annual inflation expectations are averaging 2 percent. We would not wish to see inflation expectations become unstable and decline significantly.

Monetary policy is highly accommodative and the OCR is back to historic lows. Since the beginning of 2016, the New Zealand dollar has depreciated by around 4 percent on a trade-weighted basis and market interest rates have declined. Some further exchange rate depreciation is desirable given the ongoing weakness in export prices.

We believe that imbalances in the Auckland property market pose a financial stability risk. Record low interest rates, along with record net migration inflows, strong bank lending, heightened investor activity, and insufficient housing supply have led to strong house price inflation in Auckland and an average house price to income ratio over 9.5 that is 70 percent higher than in the rest of the country. In addition, house price inflation has been accelerating in Waikato/Bay of Plenty, Northland and in Central Otago.

Recent indicators suggest that housing activity in Auckland may be beginning to slow as a result of the Government’s measures introduced on 1 October 2015 and the macro-prudential policy measures applying to investor-related lending. We will have a better feel for this when we see the February and March 2016 housing data. Nevertheless, the Bank’s macro-prudential policies have played an important role in reducing the risks associated with the growth in bank lending. Across the banking sector the share of high LVR lending (LVRs of 80 percent or higher) has fallen from 21 percent of overall housing lending before the introduction of LVRs, to 13 percent currently.

Looking ahead, monetary policy will continue to be accommodative. With the ongoing weakness in commodity prices, and particularly oil, it will take longer for headline inflation to reach the target range. On the other hand, the data on core inflation and inflation expectations are more encouraging in terms of consistency with the PTA.

However, most of the risks facing the economy are downside ones. Important amongst them is a rising concern about the strength of the global economy and increased financial market volatility. This reflects several factors, including the importance of growth in China and other emerging markets, tensions in oil and other commodity markets, and the prospect of increasing divergence between monetary policies in the major economies.

In addition to the powerful structural forces that are reducing global inflation, our economy has been hit by several important supply-side shocks. These include falling oil and dairy prices, strong net migration flows and rising labour force participation. Some, such as the changes in oil prices, net migration and participation, are positive for growth, but all of the supply shocks are exerting downward pressure on inflation in New Zealand.

These issues and the requirements in the PTA in respect of asset prices, financial stability and efficiency and volatility in output, interest rates and the exchange rate, mean that there is much to consider in determining monetary policy that extends well beyond the current level of headline inflation. If concerns deepen around the prospects for the global economy and its impact on New Zealand, some further policy easing may be needed over the coming year to ensure future average inflation settles near the middle of the target range. We will continue to monitor closely the emerging economic and financial data.

Concluding Comment

The outlook for the New Zealand economy looks positive, with growth forecast to increase to an annual rate of 3 percent and inflation projected to move back within the target band. However, there are greater uncertainties around the economic outlook than normal, and the balance of risks lies on the downside. Foremost among these risks are the difficult external environment, weak commodity prices, and unusually strong net migration flows.

In managing economic risks and assessing monetary policy we will continue to draw on the flexibility contained in the PTA and avoid taking a mechanistic approach to interpreting the PTA. A mechanistic approach could lead to an inappropriate fixation on headline inflation. It would cut across the flexibility deliberately built into the PTA framework and risk creating serious distortions in the financial system, housing market and broader economy.

[1] M Obstfeld,“The Global Economy in 2016”, IMF Survey Magazine, January 2016.

[2] Financial Times,“Capital Flight from China worse than thought”, January 20, 2016.

[3] Several developments illustrate this: policy rates are close to zero in most advanced economies, and negative in some; quantitative easing by the ECB and BoJ last year was the highest since 2011; sovereign bond yields in several countries - mainly in Europe - are currently negative for 2 year maturities and in some cases 5 year maturities; the policy rate at the Bank of England is the lowest since its inception in 1694; prices of financial assets and real estate surged to record levels in many countries; Switzerland sold 10 year bonds at a negative yield, and Mexico twice issued 100 year foreign-currency bonds that were heavily oversubscribed.

[4] OECD Economic Outlook; November 2015, page 19.

[5] P Turner, The Financing of Emerging Markets Non-Financial Companies, BIS note to G20 Finance and Central Bank Deputies Meeting, 14 December 2015.

[6] ‘OECD Economic Outlook’, November 2015, pages 27-28.

[7] D Ford, A Wood,‘El Niño and its impact on the New Zealand Economy’, RBNZ Analytical notes AN2015/07, December 2015

[8] G Price ‘Some Revisions to the sectorial factor model of Core Inflation’, RBNZ Analytical Notes, AN 2013/06, October 2013