Address to the New Zealand Credit and Finance, Rotorua

1. Introduction

The New Zealand economy has grown strongly over the past four years. Initially concentrated in the export sector, this expansion gradually shifted toward the domestic economy. While a sustained expansion in economic activity is obviously pleasing, we have also seen some significant `excesses' develop in the economy. Productive resources have become severely stretched, which has led to an increase in inflation pressures. There has also been a widening in New Zealand's current account deficit -- the difference between what the country earns overseas from its exports and investments and what it pays for its imports and the investments foreigners have in New Zealand. These two developments largely share a common underlying driver -- very strong growth in spending, particularly by the household sector, much of which has been debt-financed.

2. Looking at the imbalances

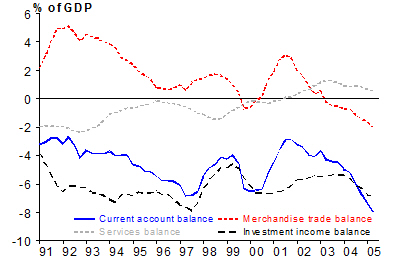

Figure 1 : Current account deficit reaches 8% of GDP

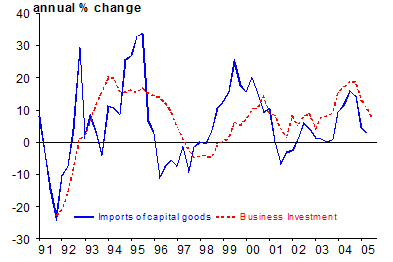

Some of the drivers of the recent current account deficit are not necessarily a cause for major concern. New Zealand has been undergoing a strong business investment cycle which has necessarily meant high demand for imports of capital goods, which we can't or don't produce locally. Investment is obviously necessary for sustaining future growth in activity. The profits paid on foreign investment in New Zealand have also been growing, due to the relative strength of many parts of the economy.

Figure 2 : Businesses importing capital goods

But while some components of the current account simply mirror cyclical strength in the economy and the efforts of businesses to increase their long-term productive capacity, the widening deficit has also reflected very strong spending on part of the household sector. At a time when government and the business sector have increased their savings (with growing fiscal surpluses and higher profits), household savings has continued to decline.

During the past few years, we have seen very sharp rises in house prices in New Zealand, reflecting strong demand by New Zealanders and overseas investors alike. Associated with this buoyancy in the housing market has been a strong tendency among many households to `unlock' housing equity built-up through capital gains to fund consumption. This often involves borrowing more against the equity in the home. Rising house prices have boosted the perceived wealth of home-owners and, along with an increased access to debt, have underpinned very strong consumption spending. Strong consumption spending has in turn fuelled much of the demand for imports that has led to a widening of New Zealand's trade deficit.

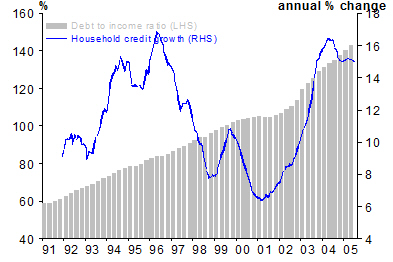

In effect, we have seen a continued decline in the New Zealand household savings rate -- the proportion of current income that households put aside to invest for future consumption. Statistics New Zealand figures suggest that on average households in New Zealand do not actually save anything out of current income but instead dis-save to the tune of around 12 per cent of income per annum. Of course, there is plenty of room to debate whether this is the most relevant or accurate saving statistic.1 But comparative figures show that, typically, households in most developed countries save at least some of their current income. It is clear that the New Zealand household sector stands out as having one of the lowest savings rates of any OECD country.

Figure 3 : Household credit growing faster than income

It is possible that households' expectations of the capital gains from housing have been so strong that many households have seen scope to unlock recent capital gains, whilst still expecting to be able to build up their equity sufficiently over the long-run to meet their savings goals. If so, they would have seen little need to save anything out of current income. Obviously the success of this strategy will depend on the extent to which house prices do in fact continue to rise from here. The Reserve Bank has noted several times in the past few years that some households may have had unrealistic expectations in this regard; indeed a fall in house prices cannot be ruled out. In Australia house prices today are, if anything, lower than they were a year ago, certainly so in Sydney.

We are also conscious that there may be subtle changes occurring around what households regard as an acceptable target level of wealth in retirement. This may be driving current consumption and savings decisions. Traditionally, the bequest motive has been a driver of many New Zealanders' savings strategies. Some baby-boomers may be opting to spend more of their accumulated wealth during their lifetime and not make a significant bequest. It is also possible (but hard to gauge) that some households have viewed the recent increase in government savings (i.e. fiscal surpluses) as a sign that they can afford to save less themselves.

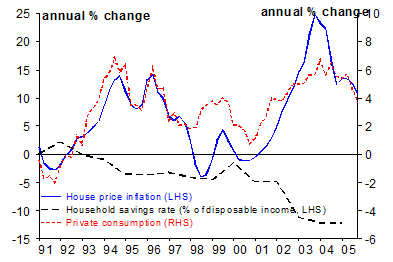

Figure 4 : Households consuming from debt

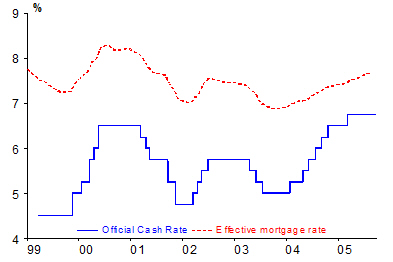

Recourse to debt-financing has been an important part of the process. Despite an Official Cash Rate that has been high by international standards, households appear to have been very willing to increase debt levels to fund their housing and consumption activity. Strong competition among home loan providers -- which has meant lower home loan rates than might otherwise be the case -- has certainly done little to discourage households in this regard. In some cases, interest rates for fixed-rate home loans appear to have been priced below the all-up cost of lending, as lenders have competed for market share. Lenders have clearly seen home loans as a relatively low risk activity and have priced loans accordingly.

Figure 5 : Effective mortgage rate

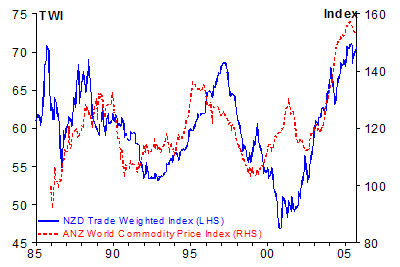

Household behaviour is not the only influence on the current account. The rise in the exchange rate over the past few years has reflected rising commodity prices, New Zealand's strong relative growth performance and our correspondingly higher interest rate structure relative to the rest of the world. The high exchange rate has reinforced the widening of the current account deficit, placing pressure on export sector revenues, whilst making imports relatively cheaper. Although the factors behind the appreciating exchange are easy to identify, what has been surprising has been the continued willingness of investors to continue investing in New Zealand dollars through the likes of Eurokiwi and Uridashi2 issues notwithstanding a growing consensus that the exchange rate has reached unsustainable levels. Over the past year alone, we have seen an additional $20 billion of such issues, and demand has continued to remain very strong in recent months. Flows into these two particular products were larger than was the case for any other currency.

Figure 6 : NZD since float

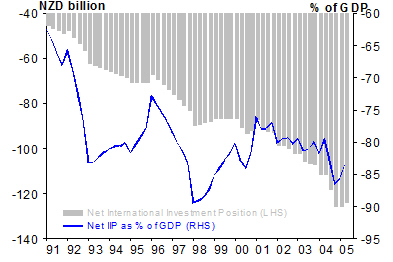

New Zealand is not the only country to have experienced a widening of its current account deficit in recent years. A number of others, including the US and Australia have also experienced widening deficits. Strong household demand has likewise been an important driving factor behind the increases although, as in the case of New Zealand, not necessarily the only factor. However, New Zealand stands out in one important respect. Over time, current account deficits have to be financed either through equity investment by foreigners or by borrowing from overseas. New Zealand's foreign liabilities currently outweigh its foreign assets to the tune of $124 billion (81 per cent of GDP) a much higher net liability position than in virtually any other developed country. This reflects our long history of running current account deficits.

Figure 7 : New Zealand's Net International Investment Position

3. The adjustment process

Currently standing at 8 per cent of GDP, New Zealand's current account deficit is at levels that cannot be sustained indefinitely. Doing so would imply a continued increase in New Zealand's indebtedness, and debt servicing costs, relative to the income available to service that debt (i.e. its GDP). History tells us that at some point the deficit will `correct' back to lower levels.

The process of current account correction is likely to involve some combination of an expenditure reduction through lower domestic demand and expenditure switching away from imported goods towards locally produced goods and services. It is also likely to involve an increase in exports. Such adjustments are likely to be prompted by a lower exchange rate and/or higher interest rates. The transition to a lower current account deficit effectively means reducing New Zealand's reliance on foreign savings and increasing the saving we do ourselves. For the household sector, which has been relying heavily on debt in order to finance spending, this adjustment process may not be painless. A correction in the housing market -- a slowing in house price inflation or even an outright fall in prices -- is likely to be part of this process.

A reduction in the exchange rate from its current high level is likely to be an integral part of the adjustment process. Significant parts of the export sector, such as manufacturing and services have been under pressure, while those supplying local markets have faced considerable competition from falling import prices. There also appears to be a growing sense among analysts and commentators that the exchange rate is materially overvalued and that a substantial fall is both desirable and inevitable at some stage in the next couple of years.

No one can reliably predict when the exchange rate will decline nor what path it is likely to take. Factors outside our control -- including the path of the US dollar -- could have a significant bearing on developments. It should also be emphasised that even once the exchange rate begins to fall, an increase in exports and a reduction in imports will not occur instantaneously. Export markets take time to rebuild and consumer buying patterns take time to respond to changes in relative prices.

Although projecting when the exchange rate may begin to head lower is a difficult task, the likely precursors for such an adjustment seem clear. As the current account deficit continues to increase, one would expect the foreign providers of capital to re-assess the relative exchange rate risk attached to their investments in New Zealand dollar assets, increasingly recognising that the exchange rate cannot be sustained at current levels. In addition, a slowing domestic economy is likely to see expectations of future returns on such investments being revised down.

4. Why is the Reserve Bank concerned about all of this?

The Reserve Bank's interest in the current account deficit, and its associated macro-economic effects, stems from our key areas of responsibility:

- Our role in helping to maintain macro-economic stability. The Bank is required to maintain price stability whilst avoiding unnecessary instability in interest rates, exchange rates and output; and

- Our financial stability role. The Bank is obliged to make sure the financial system remains resilient in the face of imbalances (such as a large current account deficit and growing debt levels) and subsequent adjustments that might occur.

We will say more about our financial stability role when we release our next Financial Stability Report in November. While we believe the New Zealand financial system is well placed to weather strains that may be borne by its customers, we will be monitoring the risks closely as we go forward.

On the price stability front, we are required to maintain inflation within the 1 to 3 per cent target band `on average over the medium term'. That task has been particularly challenging of late due to several factors:

- As noted, household demand has remained very strong over recent times, despite relatively firm monetary policy settings. Consequently, inflation pressures have remained strong in many parts of the domestic economy, including housing and construction.

- The recent sharp rise in world oil prices is putting upward pressure on inflation as higher petrol prices `at the pump' and the effects of higher fuel prices risk becoming entrenched in inflation expectations. At the same time, we are expecting these increases to exert a dampening effect on household and business demand. Estimating the balance of these effects is difficult.

- The likelihood of a more expansionary fiscal policy over the coming period has the potential to add inflation pressure in what remains a rather stretched economy. A growing fiscal surplus has clearly made higher levels of government expenditure affordable in the longer term. However, in the short-term, a more expansionary fiscal stance also has the potential to aggravate the current account deficit as well as increasing the work monetary policy has to do in order to contain inflation. These pressures will need to be borne in mind as the incoming government considers its fiscal options.

We are conscious that the eventual adjustment of the high current account deficit could make the job of maintaining price stability more difficult in these circumstances. In the short-term, an exchange rate adjustment has the potential to boost inflation via its direct effect on tradables prices. How problematic this might be for monetary policy would largely depend on the timing and magnitude of the exchange rate adjustment, which is something over which the Bank has little control. A falling exchange rate in the context of continued strength in domestic spending would tend to generate stronger inflation pressures. Conversely, the inflationary effects of an exchange rate decline that occurred following a cooling in domestic demand are likely to be more easily managed.

As far as possible, the Bank will not stand in the way of an exchange rate adjustment, accepting that a short-term boost to tradables inflation may be an unavoidable consequence of adjustment. Clearly, a more orderly and gradual exchange rate adjustment would pose less of a challenge for monetary policy. However, whatever the adjustment path, our job will be to focus on medium-term inflation stability. The extent to which monetary policy will need to continue leaning against domestic inflation pressures will largely depend on the spending and savings behaviour of households.

5. Conclusion

Strong household demand associated with a buoyant residential property market has contributed to an increase in inflation pressures and a widening of New Zealand's current account deficit. The Reserve Bank remains focussed on ensuring that the inflation outlook remains consistent with the medium term target whilst recognising the macro-economic adjustments that are likely to occur in the face of a large and unsustainable current account deficit. We are concerned to see that, as far as possible, such adjustments occur in as orderly a manner as possible.

1 For example, the blurred boundary between households and firms these days might suggest that total private savings, including by firms, is more relevant. Another issue is that saving is measured as the difference between income and consumption, making it prone to measurement error in either of those aggregates.

2 See Drage, D, A Munro and C Sleeman `An update on Eurokiwi and Uridashi bonds', Reserve Bank of New Zealand Bulletin, 68/3, September 2005.