The MPC sets monetary policy in pursuit of its economic objectives: to achieve and maintain stability in the general level of prices over the medium term; and to support maximum sustainable employment. Guided by its Risk Appetite Statement and Principles governing monetary policy tools, the MPC chooses the combination and settings of monetary policy tools necessary to achieve the amount of monetary stimulus required to achieve its objectives.

In March 2020, the MPC launched a Large Scale Asset Purchase (LSAP) programme as part of its broad monetary policy response to the COVID-19 pandemic. The MPC stopped these purchases in July 2021.

The MPC’s assessment of the LSAP tool against its principles is noted in table 2.1. When the MPC launched the LSAP programme, its principles led to the adoption of a front-loaded and dynamic approach to asset purchases. This approach helped deliver stimulus effectively and efficiently when needed, and stabilised important financial market channels of monetary policy by providing the financial system with additional liquidity.

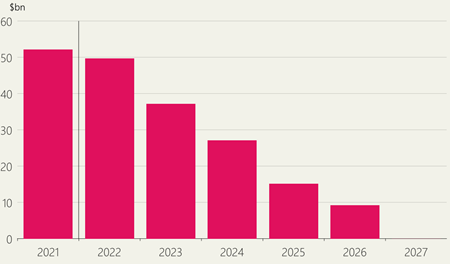

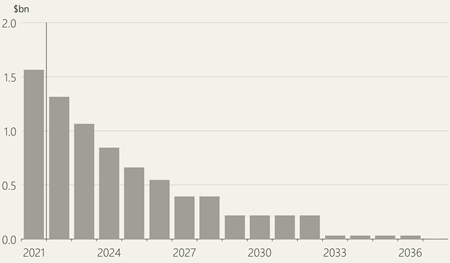

When applying its principles in the current environment, the MPC has decided to adjust monetary stimulus primarily using the OCR. LSAP bond holdings will not be dynamically used to adjust monetary stimulus. Sales of bonds in addition to maturities will be done gradually and predictably to maintain market functioning and avoid unnecessary volatility in interest rates. The MPC acknowledges that bond yields may adjust as the bond holdings are reduced, and is comfortable that any changes will be orderly and not undermine the desired stance of monetary policy. A gradual and predictable reduction in bond holdings is also consistent with how other central banks intend to reduce their asset holdings. The expected path of the two LSAP portfolios are presented in figures B1 and B2.

Figure B1: Expected LSAP portfolio of New Zealand Government bonds

(holdings as at calendar year end)

Source: RBNZ estimates.

Note: Includes nominal and inflation-indexed New Zealand government bonds. Sales are in addition to bond maturities and are expected to begin in mid-2022.

(holdings as at calendar year end)

Source: RBNZ estimates.

| Adding stimulus (buying bonds) | Removing stimulus (bonds maturing and selling bonds) |

|

|---|---|---|

| Effectiveness | Objective of purchases is to lower and flatten the yield curve; purchases front-loaded and adjusted dynamically |

Objectives of maturities and sales are to have minimal impact on monetary stimulus; undertaken gradually and predictably |

| Efficiency | Purchases and sales to be undertaken while minimising unnecessary volatility and distortions in financial markets |

|

| Bonds purchased in the secondary market | Bonds sold to New Zealand Debt Management (NZDM) or allowed to mature with no reinvestments | |

| Financial stability | Purchases help to restore market functioning and provide liquidity | Maturities and sales undertaken gradually and predictably to maintain market functioning |

| Public balance sheet risk | The MPC is guided by the Reserve Bank’s internal financial risk appetite, institutional arrangements and indemnities from the Crown. As required under the indemnity, throughout the programme the Reserve Bank has coordinated with NZDM to ensure that the objectives of both the MPC and NZDM can be achieved. | |

| Operational readiness | The Reserve Bank is operationally ready to undertake both bond purchases and sales on behalf of the MPC, and undertake necessary market operations to manage liquidity in the financial system. | |