Introduction

The Deposit Takers Bill will replace the existing prudential regulatory regime contained in the Banking (Prudential Supervision) Act 1989 and the Non-bank Deposit Takers Act 2013. The integration of these previously separate regimes will create a single, consistent framework for the regulation and supervision of financial institutions that essentially engage in the same activity — the business of taking ‘deposits’ from the public, and lending to individuals, households, and businesses. This will be a major change to the way we work as the prudential regulator and for industry.

We plan to consult extensively during the implementation period. Details of the planned consultations can be found in the CoFR Regulatory Initiatives Calendar.

View the Q1 2023 calendar on the CoFR website (PDF 885 KB)

The key areas of focus for the Reserve Bank in implementing the Bill are:

Download the Deposit Takers Bill pie chart (jpg, 169 KB)

New prudential standards for deposit takers and the proportionality framework

The Deposit Takers Bill will modernise and enhance the prudential regulation of deposit taking institutions. Prudential standards are the primary legal mechanism by which prudential requirements will be imposed on deposit takers. Standards aim to ensure that risks to the soundness of deposit takers and the financial system are appropriately managed.

These standards are secondary legislation and will replace the current conditions of registration model (for banks) and regulations (for NBDTs). The Bill sets out the subject matter of the standards, the procedure for issuing the standards, and a number of decision-making principles to be applied in developing the standards (for example, the desirability of proportionality, competition, and avoiding unnecessary compliance costs).

The development of these standards will be a major feature of our prudential policy work programme in the coming years, and will be subject to several rounds of public consultation. There will be an intensive process to translate the respective bank and NBDT rulebooks to standards, in order to have the rules ready to relicense existing deposit takers under the new legislation (and to license any new applicants).

In most areas, we are not envisaging a fundamental redesign of all our existing rules for banks that are already subject to regulation by the Reserve Bank, but there will be areas where our rules need to be updated to reflect the new law, and opportunities to clarify and simplify the rules in some instances. For NBDTs, the existing rules to which they are subject will also be considered to ensure some degree of consistency across the sector, albeit balanced with taking a proportionate approach (see below). There will be substantial engagement with industry as we develop the new rules. NBDTs are currently supervised by trustees; however, when the Bill is passed the Reserve Bank will assume this responsibility.

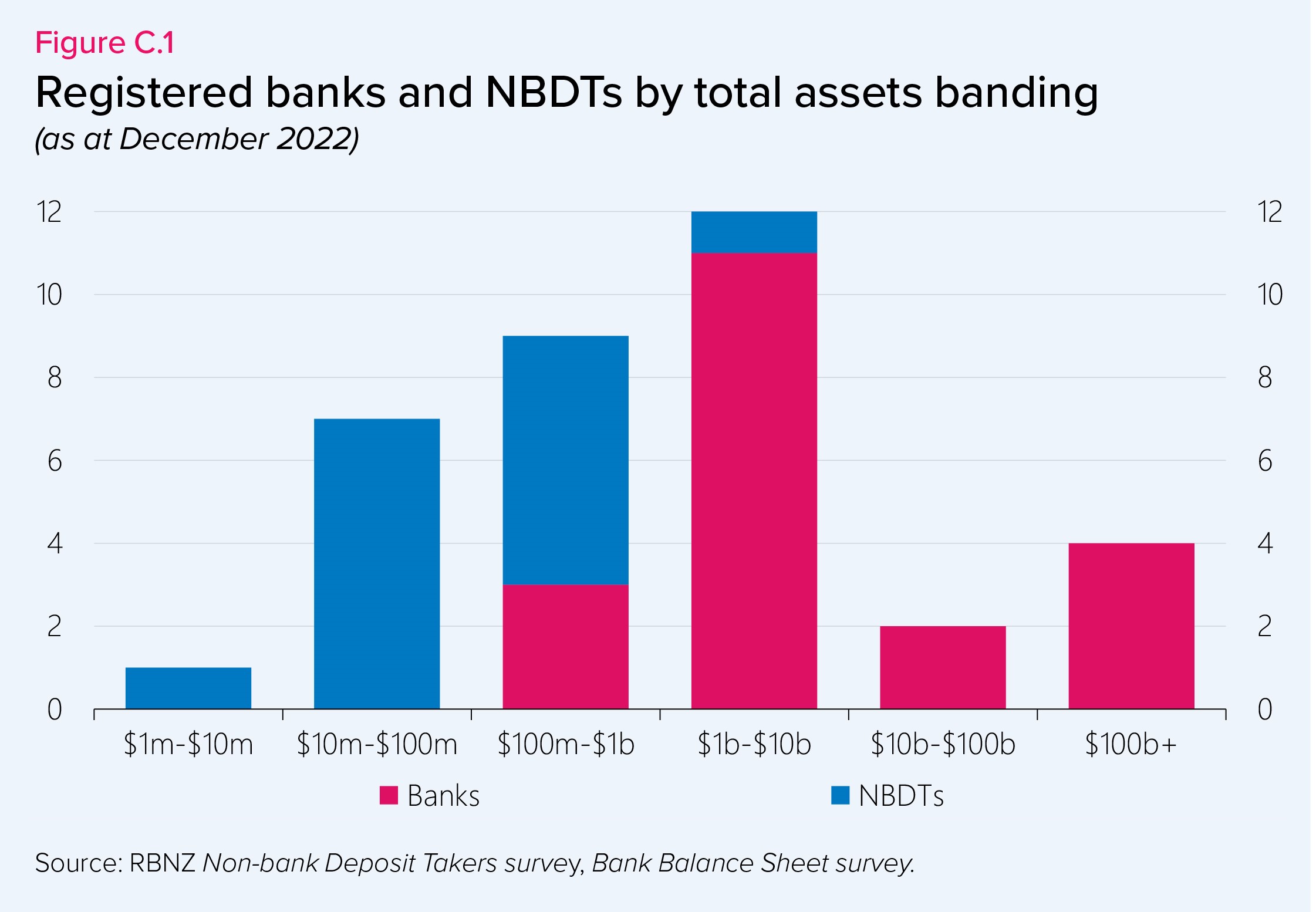

A single regulatory regime means that we must design prudential standards and other regulatory tools that have proportionate requirements for the wide spectrum of deposit takers. We do not envisage the prudential rules as being ‘one size fits all’, and will be thinking carefully about creating rules that are suitable for the size and other characteristics of these entities, while ensuring the soundness of individual deposit takers.

Based on current data, NBDTs account for just over $3 billion in assets, out of around $658 billion in total deposit taker assets. Within the NBDT sector itself, there is a wide range of entities, ranging in size from $1 billion to the smallest at $4 million.

To help facilitate a consistent and transparent approach to proportionality across a wide range of standards, we are developing a proportionality framework. The value of the proportionality framework in the development of new standards is that it can assist in calibration where simpler, but still strong, requirements are warranted.

As indicated in the CoFR Regulatory Initiatives Calendar, we intend to consult on the proportionality framework later this year.

{kind=link}

Download the graph showing registered banks and NBDTs by total assets banding (jpg, 221 KB)

{kind=link}

New Depositor Compensation Scheme (DCS)

The DCS will protect deposits up to $100,000 per eligible depositor, per licensed deposit taker. ‘Protected deposits’, as defined under the Bill, will include New Zealand dollar deposits in transactional accounts, call accounts and savings accounts, and term deposits (and equivalent products) issued by licensed deposit takers. The DCS is a significant new initiative for New Zealand, and function for the Reserve Bank. There are significant implications for deposit takers as well, including the development of ‘single customer view’ files to support the accurate identification of depositors eligible for compensation.

The Minister of Finance has indicated his intention for the Scheme to commence operation in late 2024. To support this, the Treasury and Reserve Bank will consult on a range of funding and levy related policies this year.

New resolution framework

The Bill provides an updated crisis management and resolution framework and establishes the Reserve Bank as the Resolution Authority for all licensed deposit takers. The new framework contains additional purposes for the Reserve Bank to pursue in its role of Resolution Authority, and provides for additional protections for creditors, in line with international practice.

Under the Bill, the Reserve Bank will be required to publish a Statement of Approach to Resolution, setting out our expected strategies for dealing with failing deposit takers, and our intended approach to co-operating and engaging with relevant agencies, both domestically and internationally. To support this, the Reserve Bank is currently undertaking policy work to explore optimal resolution strategies for different cohorts of deposit takers. This work will include a further consideration of the potential role for statutory bail-in powers, upon which we are expected to report back to the Minister of Finance within two years of the enactment of the Bill.

Licensing deposit takers

All ‘deposit takers’ will need to be licensed under the new standards issued under the Bill. There will be a transitional period from the current to the new licensing regime. It is envisaged that ‘core standards’ (those needed for licensing) will be consulted on first, to allow licensing and re-licensing to commence.

New enforcement tools

The Bill establishes new criminal offences, civil pecuniary penalty liability and infringement offences for the breach of requirements imposed by, or under, provisions contained in the Bill. The enforcement tools in the Bill are designed to provide a range of options that will allow for a proportionate, risk-based, and transparent response. Our Enforcement Framework sets out the considerations that apply when we select matters for investigation, conduct investigations, and ultimately make decisions relating to enforcement matters.