This article describes how the Reserve Bank analyses international shocks and their implications for monetary policy. As a small open economy, New Zealand is particularly vulnerable to international shocks. The Bank has a long tradition of using a wide range of models to assess the impact of different types of international shocks and their spillovers to New Zealand through various channels. This modelling has explored the transmission of these shocks through trade, financial, and confidence or uncertainty linkages. As the international economy and financial markets continue to evolve, the Bank will continue to refine its modelling strategy to better understand how these shocks evolve and transmit through to the domestic economy.

1 Introduction

As a small open economy, New Zealand is vulnerable to the impact of unexpected global economic events. These events, or shocks as they are called by economists, can either affect many countries simultaneously (i.e. a global shock), or originate in one country and transmit to other countries (i.e. spillovers). Higher oil prices are an example of a global shock, while the effect of US quantitative easing on other countries is an example of a spillover. Global shocks and spillovers have increasingly become an important feature when setting monetary policy (Georgiadis, 2016, Potjagailo, 2017). The outlook for the international economy has been a key focus recently, with trade tensions, volatile financial conditions, and rising uncertainty all creating risks to growth. Therefore, policymakers need to be aware of international linkages when setting monetary policy.

This article describes how the Reserve Bank analyses international shocks and their implications for monetary policy. A wide range of models are used to assess the impact of different types of shocks and spillovers through various channels.

The rest of the article is organised as follows. Section 2 describes the links between the New Zealand economy and the international economy. Section 3 reviews the literature on the relationship between domestic monetary policy and international shocks. Section 4 summarises some of the modelling tools used by the Bank to analyse the impact of international shocks. Section 5 provides a conclusion.

2 New Zealand’s links to the international economy

New Zealand has become increasingly exposed to international shocks over time as global links have strengthened. There are several reasons for New Zealand’s increased exposure to international shocks. Structural changes, such as the liberalisation of trade and capital movements since the 1980s, have increased cross-border financial flows and trade volumes. There have also been more recent factors since the global financial crisis, such as the unconventional monetary policy stimulus in major economies, that have affected the rest of the world.

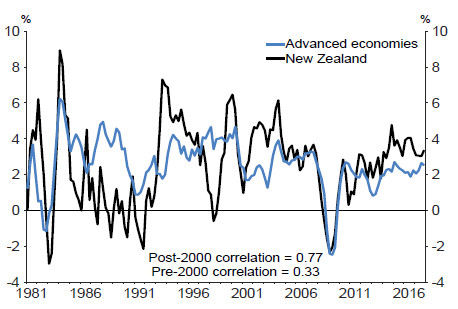

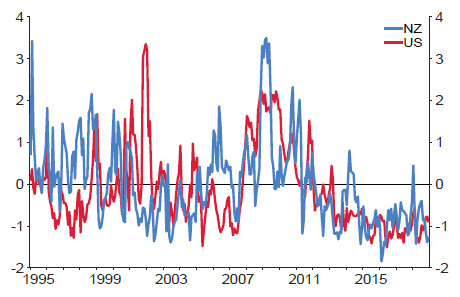

New Zealand’s closer connections with the rest of the world can be seen in the co-movement of key economic variables. With more open global markets, developments in major economies can have substantial impacts on the rest of the global economy, including New Zealand. New Zealand’s economic growth has become increasingly synchronised with that of advanced economy trading partners (figure 1). Trading-partner growth is an important driver of demand for New Zealand’s goods and services. Exports amount to around 30 percent of New Zealand’s Gross Domestic Product (GDP).

Figure 1: New Zealand GDP growth and advanced economies growth (annual)

Source: Stats NZ, Haver Analytics, RBNZ. Note: Advanced economies are an equal weighting of US, Australia, and euro area growth.

Figure 2: NZ and international long-term interest rates

Source: Bloomberg, RBNZ.

Figure 3: Daily co-movement between 10-year NZ and US government bond yields (correlation coefficient)

Source: Bloomberg, RBNZ estimates.

Figure 4: policy rates

Source: Bloomberg, RBNZ

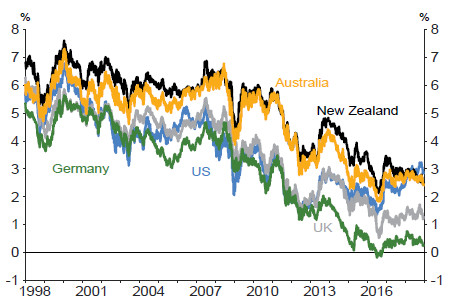

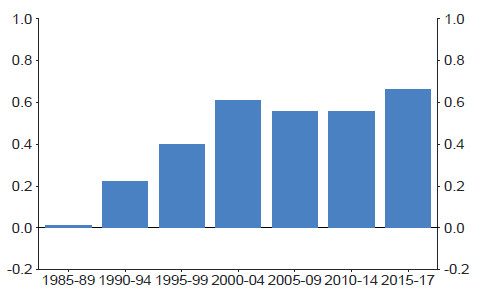

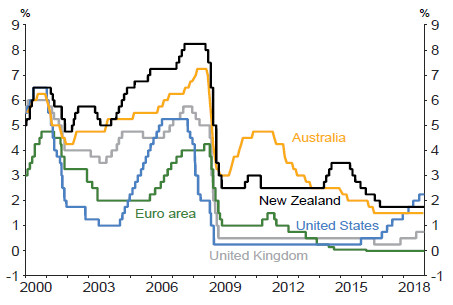

Long-term government bond yields have also tended to move together across countries (figure 2), and the correlation between New Zealand and US bond yields has increased over recent decades (figure 3).2 During the global financial crisis, cuts in policy rates were also closely aligned as central banks aimed to support their economies simultaneously (figure 4). Changes in wholesale interest rates flow through to costs of borrowing for New Zealand firms and households, which can affect economic growth and inflation.

3 International shocks and monetary policy

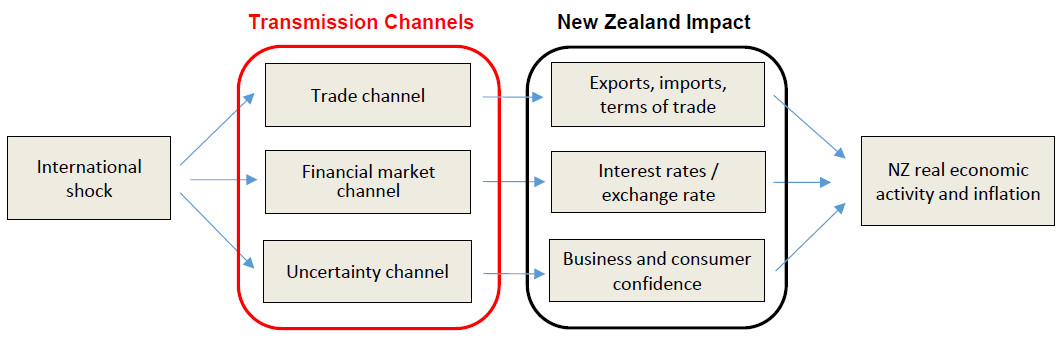

International economic shocks can affect small open economies such as New Zealand through several channels. These channels are often split into three categories − trade, financial market and uncertainty (or confidence) channels − that are summarised in figure 5.3

Through the trade channel, an international shock can affect demand for New Zealand’s goods and services exports, which can impact the quantity sold and the price. Depending on the nature of the shock and its relative impact on export and import prices, the impact on New Zealand’s terms of trade (the ratio of export prices to import prices) could be either positive or negative.

The impact through the financial market channel is mainly through interest rates and the exchange rate. As noted in the previous section, movements in New Zealand interest rates are highly correlated with movements in other countries. The correlation is particularly high for long-term interest rates, whereas short-term rates are more influenced by expectations for monetary policy settings in each respective country.4 Developments in financial markets can also impact bank funding costs and spreads through international assessments of risk.

Finally, international shocks can affect New Zealand through uncertainty or confidence channels. For example, the prospect of changes to international tariffs can make businesses and households more uncertain about their future income or employment, and cause them to cut spending and increase their precautionary savings.

Figure 5: Transmission channels of international shocks to the new Zealand economy

An international shock can impact the New Zealand economy through any combination of the three channels described above, depending on the nature of the shock. The channels can also interact to produce compounding effects. For example, lower export prices and terms of trade can also lower the exchange rate, which could affect business and consumer confidence.

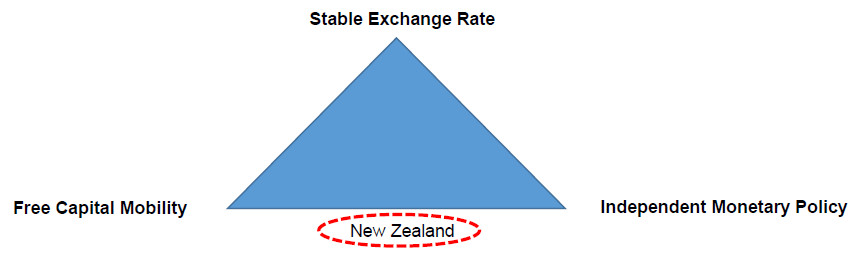

The impact of international shocks on monetary policy settings depends on a central bank’s priorities and objectives. The options for policymakers are usually summarised by the ‘Trilemma’ or the ‘Impossible Trinity’.5 According to the trilemma, when facing shocks, a central bank or government can choose two, but not all three, from exchange rate stability, independent monetary policy and an open capital account (figure 6).

The combination of macroeconomic priorities chosen depends on an economy’s circumstances. For example, many developing economies that rely on exports and have under-developed financial markets, prefer to maintain exchange rate stability and monetary policy independence, but not free capital mobility. Most advanced economies, such as New Zealand, choose to have monetary policy independence and free capital mobility. This means accepting greater exchange rate variability. A benefit of the latter choice is that exchange rate movements can act as shock absorbers in response to international shocks. For example, if export prices fall, the negative impact of this shock on the New Zealand economy can be partly offset by allowing the exchange rate to decline.

The trilemma framework has been widely used to analyse the options available to policymakers for responding to international shocks. However, this framework may be less relevant in a world of integrated capital markets. Empirical work by Rey (2013) suggests capital flows between countries are largely driven by factors such as international risk appetite and US monetary policy settings. As a result, a floating exchange rate regime may not be enough to ensure monetary policy independence, as suggested by the trilemma. In this case, the trilemma of policy choices collapses to a ‘dilemma’ between having monetary policy independence with restrictions on capital movements, or having free capital movement. More recent analytical work on whether the trilemma of policy choices still applies. Overall, the recent literature does suggest that exchange rate variability can increase monetary policy’s ability to respond to shocks.6

Figure 6: The monetary policy trilemma

4 Models used to analyse international shocks

The Reserve Bank has a long tradition of incorporating international links to the New Zealand economy into its modelling work. These modelling efforts are usually driven by a need to understand specific issues related to the New Zealand economy.

The Bank’s modelling of international links can be classified into two broad groups – ‘structural’ or theory-based, and ‘data-driven’ or statistical. Structural models are mainly based on economic theory, whereas data-driven approaches pay greater attention to explaining the data accurately. Both approaches have their strengths and weaknesses. Structural models are consistent with theoretical principles and imply clear transmission mechanisms, but sometimes they sacrifice their conformability to actual data. In contrast, statistical models can fit the data better, but this may require less theoretical consistency, which makes it harder to identify the true drivers or story behind economic developments. Picking a modelling approach often involves a tradeoff between theoretical consistency and statistical accuracy. The Bank uses a combination of structural models and data-driven models to inform its analysis.

A good example of a structural model is the New Zealand Structural Inflation Model (NZSIM) (see Kamber, McDonald, Sanders and Theodoridis, 2016), which includes the impact of international factors on the New Zealand economy. In NZSIM, the key variables that affect domestic inflationary pressure are trading partner inflation and capacity, foreign interest rates, commodity prices, export demand, and international migration. Of these foreign variables, the commodity price channel has the strongest influence. For example, scenario analysis in the Reserve Bank’s February 2017 Monetary Policy Statement showed how 4 percent higher export prices over the projection would result in the OCR increasing 50 basis points more than the central projection, all else equal. The Reserve Bank has also incorporated open economy features into other structural models. Some of these have been aimed at understanding the effect of foreign funding on the New Zealand banking system (e.g. Kamber and Thoenissen, 2013, Jacob and Munro, 2018).

Data-driven models have been more widely used than structural models to study international links at the Reserve Bank. Many of the data-driven models are variants of vector autoregression (VAR) models. VARs are estimated on multiple economic series and help to understand the links between them. Like all modelling choices, the type of VAR model chosen depends on the specific question at hand.

Trade channel

Much of the Bank’s work on the trade channel has explored the impact of changes in commodity prices. This reflects that New Zealand is a small open economy whose main link with the rest of the world is through commodity exports. Kamber, Nodari and Wong (2016) set up a VAR model to understand the effect of commodity price shocks on New Zealand economy, and find that commodity price shocks behave like demand shocks. For example, in response to a rise in commodity prices, they find that business investment, consumption and GDP increase, and put upward pressure on non-tradable inflation. However, this also puts upward pressure on the exchange rate, which causes tradeable inflation to fall, and thus the overall effect on inflation is more modest.

Osborn and Vehbi (2015) use a structural VAR model to analyse the effects of growth in China and the US on New Zealand. Their model includes an exogenous global block comprising US and China growth rates together with world real commodity price inflation. They find that growth spillovers from the US and China to New Zealand GDP play an important role in driving New Zealand’s business cycles. They also show that both foreign and domestic shocks are important drivers of New Zealand’s real exchange rate fluctuations. The authors also examine the commodity price responses to growth in each of the large economies.

Some of the analysis of commodity price movements has focused on their impact on the exchange rate, as moves in the New Zealand dollar are often correlated with moves in export commodity prices. Parker and Wong (2014) show that what causes the exchange rate to move matters. Whether the exchange rate is responding to changes in commodity prices or a shift in preferences by international investors, can have very different macroeconomic effects on the New Zealand economy. Karagedikli, Ryan, Steenkamp and Vehbi (2016) investigate the effect of exchange rate shocks on different sectors of the New Zealand economy. They find that while exchange rate shocks have an effect on the tradable sector, non-tradable sectors can also be affected.

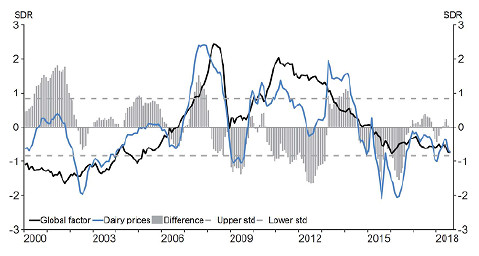

Figure 7: Global factor and dairy prices

Source: Wadsworth and Richardson (2017).

The Bank has also done modelling to understand the determinants of dairy prices, which are an important driver of the New Zealand economy. Wadsworth and Richardson (2017) use a global factor model of commodities to examine the underlying global factors driving fluctuations in dairy and meat export prices. They find that 95 and 93 percent of the movements of New Zealand’s dairy and meat export prices can be attributed to the global trend (figure 7).

Financial market channel

As a small, indebted economy with considerable international financial exposures, it is important to understand how financial market shocks in the rest of the world transmit to New Zealand. A key channel is through long-term interest rates, which are highly correlated across countries.7 A sharp increase in global long-term bond yields would generally affect a range of New Zealand interest rates, including government bond rates and swap rates. Higher long-term wholesale interest rates flow through to a higher cost of borrowing for New Zealand firms and households, which can affect economic growth and inflation.8

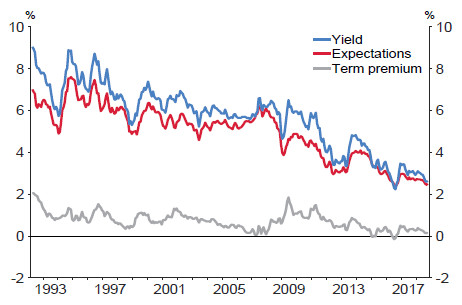

Figure 8: New Zealand 10-year government bond

Source: Callaghan (2019). Note: The expectations series is the estimated average expected policy rate over the next ten years.

Movements in long-term interest rates can be decomposed into a domestic component that reflects expectations about the future path of short-term interest rates, and changes in the ‘term premium’. The term premium is the compensation investors require for holding longterm bonds, and is often driven by global factors. Term structure models can help analyse these different drivers of long-term interest rates (Callaghan, 2019). The term premium on New Zealand 10-year government bond rates increased sharply following the global financial crisis in 2009 as investors demanded greater compensation for holding relatively risky New Zealand bonds (figure 8).9

The Bank uses a range of term structure models because different models can produce different estimates of the term premium. Term structure models can be estimated using statistical methods, such as linear regressions (eg Callaghan, 2019, Adrian, Crump and Moench, 2014), or be more structural, incorporating information from surveys on expectations (eg Halberstadt and Krippner, 2016, Kim and Wright, 2005). Term structure models can also be used to better understand market expectations of central bank policy rate moves, as term premiums can also influence short-term interest rates.10

More broadly, bank funding costs in New Zealand can be significantly affected by global risk pricing and market conditions. The Bank models and monitors bank funding costs, by considering the pricing of various spreads, wholesale debt, and retail deposits (Wong, 2012, and Cook and Steenkamp, 2018).

Uncertainty channel

Some international shocks, such as unanticipated political events, increase global uncertainty about the macroeconomic outlook.

Global uncertainty also tends to impact New Zealand via the trade and financial market channels. Global economic uncertainty can prompt delays in investment and spending, reducing global demand and demand for New Zealand’s exports. Kamber, Karagedikli, Ryan and Vehbi (2016) investigate the effect of an uncertainty shock in the US on the New Zealand economy. They find an uncertainty shock in the US acts as a negative demand shock on the New Zealand economy. Perhaps more surprisingly, the impact of an uncertainty shock in the US is an appreciation of the US dollar relative to the New Zealand dollar. This ‘flight to safety’ response to global uncertainty means that the New Zealand dollar depreciates in the event of an uncertainty shock in the US, as global investors shift to the US to mitigate increased uncertainty. Greig, Rice, Vehbi and Wong (2018) consider a range of uncertainty proxies for New Zealand and find that international measures of uncertainty are just as informative about the New Zealand economic outlook as New Zealand specific measures. In other words, economic uncertainty in New Zealand may partly reflect broader global uncertainty (see figure 9).

Figure 9: uncertainty proxies (US and New Zealand, standard deviations from mean)

Source: Consensus Economics, RBNZ calculations (see Greig et al, 2018, for details).

Larger international models

Recently the Reserve Bank has built several larger models to explore a wider range of international shocks. Two examples of these models are the Factor Augmented VAR (FAVAR) and Global VAR (GVAR) models. The FAVAR approach allows many variables to be incorporated into a model through the use of ‘factors’. A useful way to think about factors is that they summarise the co-movements of a larger group of variables. Instead of modelling all of the data series individually, a simpler approach is to reduce the large set of macroeconomic data into a smaller number of factors, which summarise the most important fluctuations in the data. Karagedikli, Mumtaz and Tanaka (2010), Kamber et al (2016), Karagedikli et al (2016), and Kamber and Wong (2018) are examples of FAVAR models.

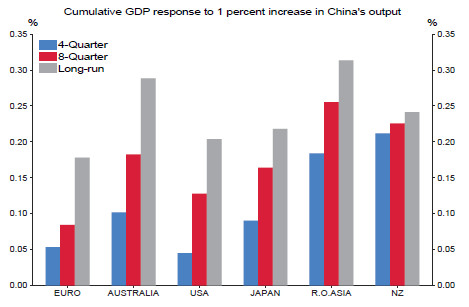

Several pieces of work have also used Global Vector Autoregression models (see di Mauro, Filippo and Pesaran, 2013). GVARs, as the name suggests, model the global economy and add a global dimension to the standard VAR framework – the countries included in the GVAR account for 90 percent of world output. Foreign variables are jointly modelled with New Zealand variables, which naturally lends itself to studying the interaction between the New Zealand economy and our major trading partners. The main advantage of the GVAR is that it can tell a rich story about international transmission through a range of channels. Figure 10 shows how a 1 percent increase in China’s GDP impacts a range of countries. As is convention in most GVAR analyses, we show the impact after four quarters, after eight quarters, and in the long run. The impact on New Zealand output is immediate and reasonably large. In the long run, the level of output in New Zealand is increased by about a quarter of a percent. In most other countries, the impact takes longer to occur, but accumulates to a similar level.

GVAR models can also be useful for producing forecasts of macroeconomic variables. Mulder and Vehbi (2018) show that GVAR is a useful addition to the range of models used by the Reserve Bank to forecast the international economy. A related piece of work by Eickmeier and Ng (2011) also reports gains from using international variables when forecasting the New Zealand economy.

Figure 10: Cumulative impacts from a 1 percent increase in Chinese GDP

Source: RBNZ calculations.

Conclusion

As financial markets and economies have become more integrated, it has become increasingly important for central banks to understand the impact of international shocks on the domestic economy when setting monetary policy. To do this, policymakers need to understand the nature of global shocks and the possible size of spillovers from the rest of the world to the domestic economy. As a small open economy, New Zealand is particularly vulnerable to international shocks. As a result, the Reserve Bank has a long tradition of modelling the impact of international shocks on the New Zealand economy. This modelling work has explored the transmission of these shocks through trade, financial, and confidence or uncertainty linkages. A wide variety of models has been used to explore these linkages. As the international economy and financial markets continue to evolve, the Bank will continue to refine its modelling strategy to better understand how international shocks evolve and transmit through to the domestic economy.

References

- Adrian, T, R Crump, and E Moench (2013) ‘Pricing the term structure with linear regressions’, Journal of Financial Economics 110(1).

- Anaya, P. and Hachula, M. (2016). ‘The dilemma or trilemma debate: empirical evidence’, DIW Roundup: Politik im Fokus 95, DIW Berlin, German Institute for Economic Research.

- Callaghan, M (2019) ‘Expectations and the term premium in New Zealand long-term interest rates’, Reserve Bank of New Zealand Analytical Note, AN2019/02.

- Callaghan, M (2017) ‘Is the market always right? Improving federal funds rate forecasts by adjusting for the term premium’, Reserve Bank of New Zealand Analytical Note, AN2017/08.

- Callaghan, M, J Culling, and A Richardson (2019) ‘Effective monetary stimulus: A measure of the stance of monetary conditions in New Zealand’, Reserve Bank of New Zealand Analytical Note, forthcoming.

- Callaghan, M and L Krippner (2016) ‘Short-term risk premiums and policy rate expectations in the United States’, Reserve Bank of New Zealand Analytical Note, AN2016/07.

- Cassino, E, N Cribbens and T Vehbi (2014) ‘Determinants of the New Zealand yield curve: Domestic vs. foreign influences’, New Zealand Treasury Working Paper, 14/19.

- Cassino, E and H Pepper (2011) ‘Making sense of international interest rate movements’, Reserve Bank of New Zealand Bulletin, 74(1).

- Chowla, S, L Quaglietti and L Rachel (2014) ‘How have world shocks affected the UK economy?’, Bank of England Quarterly Bulletin, Q2,167- 179.

- Cook, B, and D Steenkamp (2018) ‘Funding cost pass-through to mortgage rates’, Reserve Bank of New Zealand Analytical Note Series, AN2018/02.

- di Mauro, F and M Pesaran (2013) The GVAR Handbook: Structure and Applications of a Macro Model of the Global Economy for Policy Analysis, Oxford University Press.

- Eickmeier, S and T Ng (2011) ‘Forecasting national activity using lots of international predictors: An application to New Zealand’, International Journal of Forecasting, 27(2), 496-511.

- Georgiadis, G (2016) ‘Determinants of global spillovers from US monetary policy’, Journal of International Money and Finance, 67, 41-61.

- Greig, L., A Rice, T Vehbi and B Wong (2018) ‘Measuring uncertainty and its impact on a small open economy’, Australian Economic Review, 51(1), 87-98.

- Halberstadt, A and L Krippner (2016) ‘The effect of conventional and unconventional euro area monetary policy on macroeconomic variables’, Bundesbank Discussion Paper, 49/2016.

- Jacob, P and A Munro (2018) ‘A prudential stable funding requirement and monetary policy in a small open economy’, Journal of Banking and Finance, 94 (C), 89-106.

- Kamber, G and C Thoenissen (2013) ‘Financial exposure and the international transmission of financial shocks’, Journal of Money, Credit and Banking, 45, 127-158.

- Kamber G, G Nodari and B Wong (2016) ‘The impact of commodity price movements on the New Zealand economy’, Reserve Bank of New Zealand Analytical Note, 2016/5.

- Kamber, G, C McDonald, N Sander and K Theodoridis (2016) ‘Modelling the business cycle of a small open economy: The Reserve Bank of New Zealand’s DSGE model’, Economic Modelling, 59(C), 546-569.

- Kamber, G and Ö Karagedikli, M Ryan and T Vehbi (2016) ‘International spill-overs of uncertainty shocks: Evidence from a FAVAR’, CAMA Working Paper, 61/2016.

- Kamber, G and B Wong (2018) ‘Global factors and trend inflation’, Reserve Bank of New Zealand Discussion Paper Series, DP2018/01.

- Karagedikli, Ö, M Ryan, D Steenkamp and Vehbi, T. (2016) ‘What happens when the Kiwi flies? Sectoral effects of exchange rate shocks on the New Zealand economy’, Economic Modelling, 52(PB), 945-959.

- Karagedikli, Ö, H Mumtaz and M Tanaka (2010) ‘All together now: Do international factors explain relative price co-movements?’, Reserve Bank of New Zealand Discussion Paper Series DP2010/02.

- Kim, D and J Wright (2005) ‘An arbitrage-free three factor term structure model and the recent behavior of long-term yields and distant-horizon forward rates’, FEDS Working Paper, No 2005-33.

- Lewis, M and L Rosborough (2013) ‘What in the world moves New Zealand bond yields’, Reserve Bank of New Zealand Analytical Note, AN 2013/08.

- Mulder, T and T Vehbi (2018) ‘Forecasting with a global VAR model’, Reserve Bank of New Zealand Analytical Note, forthcoming.

- Mundell, R (1963) ‘Capital mobility and stabilization policy under fixed and flexible exchange rates’, Canadian Journal of Economic and Political Science, 29(4), 475-485.

- Osborn, D R & T Vehbi (2015) ‘Growth in China and the US: Effects on a small commodity exporter economy’, Economic Modelling, 45(C), 268- 277.

- Parker, M and B Wong (2014). ‘Exchange rate and commodity price pass‐through in New Zealand’, Reserve Bank of New Zealand Analytical Note, AN2014/01.

- Potjagailo, G (2017) ‘Spillover effects from euro area monetary policy across Europe: A factor-augmented VAR approach’, Journal of International Money and Finance, 72, 127-147.

- Rey, H. (2013). ‘Dilemma not trilemma: the global financial cycle and monetary policy independence’, Proceedings of the Economic Policy Symposium at Jackson Hole, Federal Reserve Bank of Kansas City.

- Wadsworth, A and R Richardson (2017) ‘A factor model of commodity price co-movements: An application to New Zealand export prices’, Reserve Bank of New Zealand Analytical Note, AN2017/06.

- Wong, J (2012) ‘Bank funding – the change in composition and pricing’, Reserve Bank of New Zealand Bulletin, 75, 15-24.

Footnotes

- 1 The authors wish to thank Paul Hutchinson, Gael Price, Adam Richardson, Christie Smith, Eric Tong, Evelyn Truong, Rebecca Williams, Fang Yao and Matthew Wright for their feedback. Since writing this article, Benjamin Wong has left the Reserve Bank of New Zealand.

- 2 For discussion about international influences on New Zealand interest rates, see Lewis and Rosborough (2013) and Cassino and Pepper (2011).

- 3 See, for example, Chowla, Quaglietti and Rachel (2014).

- 4 See Cassino, Cribbens and Vehbi (2014).

- 5 The Trilemma was first introduced by Mundell, (1963).

- 6 See, for example, Anaya and Hachula (2016).

- 7 For discussion about international influences on New Zealand interest rates, see Lewis and Rosborough (2013) and Cassino and Pepper (2011).

- 8 For example, see Box B of the February 2017 Monetary Policy Statement.

- 9 For further discussion, see Callaghan, Culling, and Richardson (2019).

- 10 See Callaghan (2017) and Callaghan and Krippner (2016).